Results 1 to 1 of 1

Thread: Pushing on Strings

Thread Information

Users Browsing this Thread

There are currently 1 users browsing this thread. (0 members and 1 guests)

LinkBack URL

LinkBack URL About LinkBacks

About LinkBacks-

05-07-2009, 12:28 AM #1Senior Member

- Join Date

- May 2007

- Location

- Asheville, Carolina del Norte

- Posts

- 4,396

Pushing on Strings

Pushing on Strings

The explosion of U.S. banks’ excess reserves since last fall illustrates the dramatic failure of monetary policy

By Gerald Friedman

May/June 2009

Dollars & Sense: Real World Economics

Monetary policy is not working. Since the economic crisis began in July 2007, the Federal Reserve has dramatically cut interest rates and pumped out over a trillion dollars, increasing the money supply by over 15% in less than two years. These vast sums have failed to revive the economy because the banks have been hoarding liquidity rather than lending.

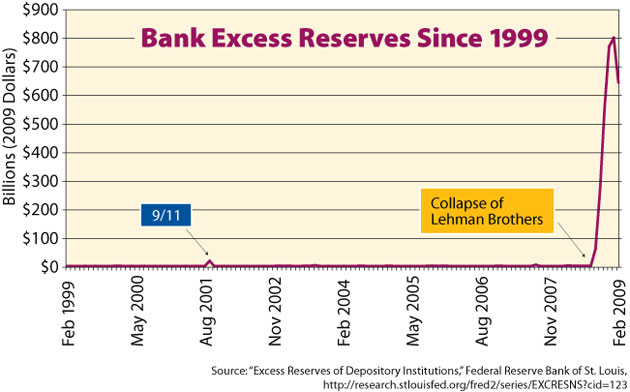

The Federal Reserve requires that banks hold money on reserve to back up deposits and other bank liabilities. In the past, beyond these required reserves, banks would hold very small amounts of excess reserves, holdings that they minimized because reserves earn very little or no interest. Between the 1950s and September 2008, U.S. banks held over $5 billion in total excess reserves only once, after the September 11 attacks. This changed with the collapse of Lehman Brothers. Beginning with less than $2 billion in August 2008, excess reserves soared to $60 billion in September and then to $559 billion in November before peaking at $798 billion in January 2009. (They have since dropped to $644 billion in the last accounting month.)

This explosion of excess reserves represents a signal change in bank policy that threatens the effectiveness of monetary policy in the current economic crisis. Aware of their own financial vulnerability, even insolvency, frightened bank managers responded to the collapse of major investment houses like Lehman Brothers by grabbing and hoarding all the cash that they could get. At the same time, a general loss of confidence and spreading economic collapse persuaded banks that there are few to whom they could lend with confidence that the loans would be repaid. Clearly, our banks have decided that they need, or at least want, the money more than consumers and productive businesses do.

Banks could have been investing this money by lending to businesses needing liquidity to buy inventory or pay workers. Had they done so, monetarist economists would be shouting from the rooftops, or at least in the university halls, about how monetary policy prevented another Great Depression. Instead, even the Wall Street Journal is proclaiming that “We’re All Keynesians Again�

Reply With Quote

Reply With Quote

Giant Laken Riley Billboard Truck Circles Biden�s Speaking Venue...

04-23-2024, 09:52 PM in Americans Killed By illegal immigrants / illegals