Results 1 to 4 of 4

Thread Information

Users Browsing this Thread

There are currently 1 users browsing this thread. (0 members and 1 guests)

LinkBack URL

LinkBack URL About LinkBacks

About LinkBacks-

11-06-2010, 12:13 AM #1Senior Member

- Join Date

- May 2007

- Location

- South West Florida (Behind friendly lines but still in Occupied Territory)

- Posts

- 117,696

U.S. Fed Buying $600 Billion in Debt with Debt

U.S. Fed Buying $600 Billion in Debt with Debt

Interest-Rates / Quantitative Easing

Nov 05, 2010 - 10:22 AM

By: Midas_Letter

Here is the glaring hole in the United States Federal Reserveâs approach to what it calls stimulus, and what history will one day categorize as fraud: You canât use your own debt to purchase more debt when you canât repay the original debt. The crime is compounded when you know youâre never going to repay the debt. It amounts to treason to intentionally destroy the integrity of the nationâs money. The Federal Reserveâs ability to âpurchaseâJoin our efforts to Secure America's Borders and End Illegal Immigration by Joining ALIPAC's E-Mail Alerts network (CLICK HERE)

-

11-06-2010, 12:16 AM #2Senior Member

- Join Date

- May 2007

- Location

- South West Florida (Behind friendly lines but still in Occupied Territory)

- Posts

- 117,696

Fed Quantitative Easing 2, One of the Greatest Blunders in History

Currencies / US Dollar

Nov 05, 2010 - 08:04 AM

By: Toby_Connor

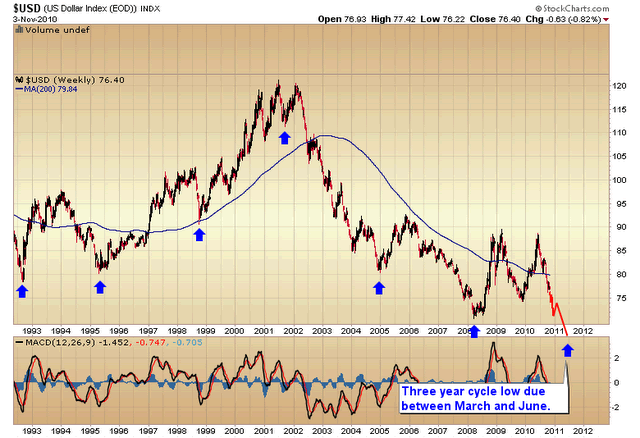

Many years from now when we look back at history I think yesterday will be seen as one of the greatest blunders ever made by a central banker.

The dollar was already headed down into a major 3 year cycle low.

The first round of QE had already guaranteed that the dollar was going to be under severe duress by next spring. Bernanke just added insult to injury yesterday and virtually guaranteed we will have a major currency crisis by next spring.

I think history will come to view yesterday as the beginning of the end for the dollar as the worlds reserve currency and unless the Federal Reserve comes to their senses soon the dollar is doomed to follow every other fiat currency in history into an eventual hyperinflation and total devaluation.

One has to protect their purchasing power from the depredations of central bankers bent on destroying the dollar. That means one has to exchange their paper dollars for real assets. It's no longer safe to hold cash.

One can buy stocks but soaring inflation will destroy profit margins and the stock market is going struggle more and more to rise in the face of soaring input costs.

There is one and only one sector that is positioned to protect one's wealth from the Fed. That sector is of course precious metals. The more the Fed devalues the better the fundamentals become. Gold is now entering the parabolic phase of this particular leg of the ongoing C-wave advance.

I doubt we will ever see sub $1300 gold again for the duration of this secular bull. Now that the HUI and silver have broken to new all time highs we have a rare condition in that the entire precious metal sector is trading in a vacuum with no real overhead resistance. This is the only sector in the world in this position. That is the recipe for an incredible move higher in a short period of time as funds begin to chase the outperformance in the precious metal sector.

The key now is to spot the top and lock in profits, but not to exit too early, and believe me most traders and investors are going to exit too early because they will try to trade this based on oscillators and overbought levels. That will be a huge mistake during a parabolic surge.

I will reopen the 15 month subscription briefly for those that want to ride the bull and need a coach to keep them focused. And for those who want a voice of reason to get you out at the top when your emotions will urge you to stay at the party too long.

Toby Connor

Gold Scents

http://www.marketoracle.co.uk/Article24051.htmlJoin our efforts to Secure America's Borders and End Illegal Immigration by Joining ALIPAC's E-Mail Alerts network (CLICK HERE)

-

11-06-2010, 12:20 AM #3Senior Member

- Join Date

- May 2007

- Location

- South West Florida (Behind friendly lines but still in Occupied Territory)

- Posts

- 117,696

Bernanke Dares The World with QE2 Money Printing

Interest-Rates / Quantitative Easing

Nov 05, 2010 - 08:16 AM

By: Brady_Willett

On November 3, 2010 the Federal Reserve Board announced another round of money printing (aka quantitative easing), and yesterday Chairman Bernanke defended the Fed's actions in the Washington Post. It is unusual for Mr. Bernanke to use the op-ed format to impart the Fed's thought process. This speaks to the fact that while so many are aware of the risks of QE2, so few see the potential benefits. Before some thoughts on QE2, first an overview of Bernanke's commentary.

Is Bernanke Disingenuous or Delusional?

Mr. Bernanke started by contending that "with unemployment high and inflation very low, further support to the economy is needed." (WP Link) http://www.washingtonpost.com/wp-dyn/co ... id=topnews

He then proceeded to laud the Fed's latest scheme:

"This approach [QE] eased financial conditions in the past and, so far, looks to be effective again. Stock prices rose and long-term interest rates fell when investors began to anticipate the most recent action." [Bolds added]

Realizing that boosting stock prices was not what the Fed claims to be the motivation behind QE2, Bernanke added that "easier financial conditions will promote economic growth", and that "lower mortgage rates will make housing more affordable and allow more homeowners to refinance. Lower corporate bond rates will encourage investment." Curiously, Mr. Bernanke did not try to explain why asset prices and interest rates have already responded to QE2 but very little (if any) benefits can be viewed with regards to the housing market and corporate investment. Rather, he ended his tortuous pro-QE2 paragraph with the following:

"And higher stock prices will boost consumer wealth and help increase confidence, which can also spur spending. Increased spending will lead to higher incomes and profits that, in a virtuous circle, will further support economic expansion."

In responding to the wild build up to QE2 - i.e. the currency wars, the threat of protectionism, and an ominous increase in commodity prices - Bernanke offers a rudimentary discussion of the wealth effect. Utterly astonishing.

Finally, in trying to portray an aura of objectivity Mr. Bernanke explored some of the potential negatives of QE2.

"Although asset purchases are relatively unfamiliar as a tool of monetary policy, some concerns about this approach are overstated. Critics have, for example, worried that it will lead to excessive increases in the money supply and ultimately to significant increases in inflation."

The so called 'critics' of QE2 have done a lot more than worry about traditional (government reported) measures of inflation (which, by definition, is an increase in the money supply), but I digress.

"Our earlier use of this policy approach had little effect on the amount of currency in circulation or on other broad measures of the money supply, such as bank deposits. Nor did it result in higher inflation."

Notice here how Bernanke tries to limit the parameters of discussion and then cherry pick a single moment in history to validate his point of view. In other words, 'don't worry about inflation because the last time we fired up the printing presses deleveraging and financial destruction all but negated the expected inflationary effects!' It would be worth calling this tact savvy if it were not for the fact that is so obviously desperate. Quite frankly, by attempting to selectively compare QE2 to QE1 Bernanke unwittingly opens a discussion that eviscerates the Fed's pretext for printing. Allow me to explain:

When the Fed first unleashed money printing in March 2009 the G-20 had just ended and central bankers were, albeit some begrudgingly, in nearly universal agreement that they would do whatever it would take to get growth back on track. Moreover, at the time asset prices (i.e. equities and housing) were falling rapidly, credit conditions were exceptionally tight, the price of gold was trading flat, and Bernanke himself was trying to justify money printing as 'credit easing' rather than quantitative easing. In short, in March 2009 money printing was warranted* and with so many global policy makers acting in unison Bernanke could print safe in the knowledge that a U.S. dollar collapse was off the table.

Flash forward to today: no major global actor (saver perhaps Japan) is on board with the U.S., and, notwithstanding the threat of deflation, there is absolutely no immediate need for emergency money printing. As for the notion that the Fed must print money to create jobs, history suggests that printing money is more linked to creating financial turmoil than producing wealth and jobs. Forget about validating this observation back to Rome, and instead consider Bernanke's preferred sampling of history - how many jobs have been created since the Fed started QE?

In short, Bernanke's commentary in the Washington Post failed miserably to explain why QE2 is a good idea. This historic op-ed has the potential to usurp Mr. Bernanke's memorable 'the Fed owns a printing press' speech as being the most preposterous.

Incidentally, what Bernanke fails to mention is that if he was in charge of almost any other central bank on the planet his policies would have already triggered a financial calamity. To be sure, USD hegemony - or the platform that allows Bernanke to dally in the land of ludicrousness - is the only topic that is worthy of discussion when the Fed elects to print. Is the very last of the last resorts, debasing the monetary unit, really justified Mr. Bernanke? It is difficult for Mr. Bernanke to answer this question given that he never asks it...

* This is not to suggest that 'money printing' is preferable to enacting sound money policies (or getting rid of the Fed completely), only that under the current system if ever the need for money printing was apparent it was in early 2009.

The Rundown On Bernanke's Smackdown

With QE2 Bernanke is essentially daring the world to get off the dollar. He has adopted this tact because he knows, or thinks he knows, that the world is not ready to abandon the dollar. For the time being Mr. Bernanke is probably right.

This said, it would be naive to conclude that the Fed is undertaking money printing because it believes that lower interest rates and rising stock prices will be the only result. Rather, the Fed's unspoken goal with QE2 is to devalue the dollar, or as James Grant put it, "the economy is not measuring up, and the Fed is going to change the ruler".

The primary danger with attempting to devalue the dollar is the dollar overshoots on the downside and/or the Fed loses its ability to print money at will. Bernanke refuses to mention much less entertain this danger directly, instead preferring to discuss 'inflation'. The problem here is that if the U.S. economy remains weak for some time, traditional inflationary pressures may seemingly stay at bay even as the foundations that support the dollar continue to be undermined by unsound monetary and fiscal machinations. Currency collapses are not forecasted by the monthly inflation readings, but instead tend to erupt from the guise of dormancy all at once.

* As the Fed prints money this provides added motivation for the global economy to seek out alternatives to USD.

Bernanke is well aware that QE2 will further motivate central bankers to explore substitutes to the U.S. dollar. For that matter, Bernanke must know that the price of gold is up by nearly 200% since he was nominated to be Fed Chairman, and that the Fed's reputation/survival is now on the line if another crisis unexpectedly arrives (due to expended all of its ammo). For lack of batter way of putting it, Ben does not seem to care. Rather, Bernanke is so blinded by the idea that preventing deflation and/or another Great Depression is his purpose in life that a resistant world is seen as merely an irritating obstacle rather than a roadblock.

If 'success' is defined by a falling dollar and potentially

dangerous/unsustainable increases in asset prices, QE2 may well succeed over the short term. However, with the haunting ruins of two historic U.S. asset bubbles in the rear view mirror, it is unlikely asset prices can rise enough to fully combat the deleveraging theme. For that matter, it is even more unlikely that the dollar can be weakened so precisely as to engender a lasting export-inspired boom. Accordingly, beyond the faint hope of launching another debt/asset bubble boom, the best Bernanke can hope for is that when the new global currency regime is being contrived the U.S. still demands a seat at the table.

The Blame Game Stops While The Speculations Continues

The sole positive to be taken from QE2 is that when the next financial crisis arrives Bernanke and company will not be able to offer inane 'savings glut' theories to deflect criticism for their irresponsible policies. To be sure, the Fed continues to print money, the Fed is encouraged that asset prices are rising as a result, and the Fed is undertaking 'huge risks' despite widespread protest. Should, and more likely when, these policies fail to produce the desired results, Bernanke will be to blame.

As for the future of USD hegemony, awhile ago I started writing a commentary on the end of USD that never made it out (a few paragraphs are posted below). I could post 5-more such speculations tomorrow, each with slightly different threads of thought, and the topic at hand would barely be scratched much less fully appreciated. The end of USD hegemony is an event like no other and, like it or not, every investor must continue to monitor what continues to look like the U.S. dollar's inevitable demise. And while perhaps still years away, thanks to Bernanke's dare we are undoubtedly much closer to the end of USD than we were on November 2, 2010.

Some notes on the end of USD Hegemony (previously unreleased and undated)

As ridiculously wrong U.S. policy makers have been about almost everything in recent decades, they would be right to start mapping out contingency plans for when the USD takes its final spin around the global economy. Extreme as it may seem, one such scenario as the dollar's days become numbered, would be to print the currency into complete oblivion, pay everyone back with these increasingly worthless pieces of paper, close the borders, and then announce a strong intention to negotiate a new currency regime. Perhaps after a few more years of laying the groundwork the U.S. - which tries to blame everyone else for their financial problems - can spin blowing up the dollar as a natural reaction to the non amiable currency policies in China.

Another option would be to use novel/ fairly unethical means to ensure debt risks are financially engineered out of existence. As farfetched as this plan might sound, remember that the U.S. government didn't run public companies and the Fed didn't own shopping malls and car loans before the crisis arrived. Is it really a stretch that the Fed becomes a covert hedge fund with unlimited powers terrorizing markets the world over to produce secretive profits? If Goldman and others can produce profits every single day why can't they Fed?

As outrageous as these policy choices might appear, it is worth noting that an unlikely long-term outcome is present trajectory - or the steady demise of America contrasted against the steady rise of other nations (i.e. China, India, Brazil, etc.). Why? Because this type of scenario - where everyone plays somewhat fairly and the least debt laden/most innovative economy wins - is a contest the U.S. no longer appears capable of winning...

BWillett@fallstreet.com

By Brady Willett

FallStreet.com

http://www.marketoracle.co.uk/Article24053.htmlJoin our efforts to Secure America's Borders and End Illegal Immigration by Joining ALIPAC's E-Mail Alerts network (CLICK HERE)

-

11-06-2010, 12:21 AM #4Senior Member

- Join Date

- May 2007

- Location

- South West Florida (Behind friendly lines but still in Occupied Territory)

- Posts

- 117,696

From QE2 To Economic Titanic, The Global Asset Inflation Surge

Economics / Inflation

Nov 05, 2010 - 01:08 PM

By: Andrew_McKillop

Ben Bernanke has cranked the U.S. Fed's printing presses one more time, with a new injection of US$ 600 billion. Market operators have responded with the only tune they know: bid up all hard asset real resource prices in the Commodities space and, for a while, also talk up their paper cousins in the Equities space, while the US dollar wilts by the hour. Not so far forward, however, this creation of virtual value will hit the iceberg of runaway asset inflation, then vast deflation, as QE2 turns to Titanic.

Examples abound. The nuclear energy asset bubble is launched and powering forward, as reactor building costs are inflated at perhaps 25 percent a year, and uranium prices have risen 26 percent in the 3 months since end-July. Oil and coal prices - if not natural gas prices which are still held back by the unsure menace of shale and frac gas resource development - are also powering forward, but with strong competition from the asset inflation now operating in nearly all and any food and soft commodities. Rubber prices, for example, are at a 30-year high. While the pretence can be maintained that commodities inflation is good news for equities, they also can be talked up, but only for a while.

With splendid and general amnesia on what this process generates, and a generous amnesty for wrongdoers who print money while pretending this is the no choice solution for an economy which wont (or can't) grow, political and economic deciders have thrown caution to the winds. Real solutions are so slow to operate, so difficult to communicate to voters and consumers, they are the collateral dead in what will be a classic inflation surge.

DISHONORING DEBT

For a while, debt servicing with debased currency will ease the heroic task of managing OECD country debt, which has grown by as much as 33 percent for some countries, since 2007. Figures for exports, but also imports will effortlessly rise as the US dollar is devalued, along with the euro and Yen and all other moneys, relative to hard asset real resources. But losers will soon be identified and subjected to especially tough treatment on sovereign debt and bond markets, triggering the renewed appearance of the IMF as lender of last resort with a special role: printing SDRs as shaky guarantees for loans of other printed moneys. To be sure, gold prices can only spiral with this buy signal, already strong in today's context.

The traditional no choice solution - hiking interest rates - can itself be wheeled on stage quite soon, if inflation is strong enough to shrink and reduce the real impact of higher rates to nothing.

At that stage, as in the 1979-1981 crisis period, interest rates and inflation can soar together, as the real economy, far below, crashes into the Titanic mass of depleted real asset values. Unlike that period however, the fat to trim and to burn inside the OECD economy is now vastly smaller, making it unsure how long the process can run, before heroic measures are needed.

Debt remains the biggest problem, so diluting it, displacing it in time and across frontiers, and finally dishonouring it are the no choice solutions for as long as economic growth refuses to come back. Here again the IMF has solutions, ranging from the eccentric to the unworkable, but produced and communicated with aplomb. Following the total failure of its directors' initiative to create a US$ 100 billion fund for green energy spending in low income Emerging economies (that is Africa - poor but growing), this fund itself being part of a supposed project for a Carbon reserve currency, the climate crisis illusion has almost completely dropped out of IMF talk. Today, as oil prices rise even if that is only in debased dollars, the IMF, teamed with other entities like the World Bank, IAEA, the OECD's NEA, the USA's Ex-Im Bank, and the OECD's Development Aid Committee can home in on energy transition to the atom as a new gambit. Unlike the green energy fund, to finance the sale of overpriced green energy vanity tech in Africa, the nuclear fund can target vastly bigger numbers: perhaps US$ 500 billion as starters.

While CO2 emissions limits and tradable chits to emit hot air lacked credibility as the bases for a new and single world money, this might be different with the atom: we can hope. National debt will be shoehorned into a range of special near-money instruments, for example uranium bonds and purchasing rights. OECD debt can exchanged for the sovereign debt of the 15 or more Emerging countries (outside China and India) who want the atom, thus exporting OECD debt and importing a slice of their growing wealth. When or if major oil exporter countries decided to play along, these energy related instruments could be extended to oil drawing or buying rights, as the program to phase out the world's current fiat moneys moves, or lurches forward.

THE PACE QUICKENS

Feats of money printing, like those of the US Fed, ECB, BOJ and all other players are called "Keynesian" but only in two senses - they do not restore economic growth and they do raise government debt. But the original version of Keynesian World Money, called Bancor, was rather close to what is de facto happening to and with world hard asset commodities. Value shifts from paper to food, energy, minerals, infrastructures and other real resources, after a dangerous and damaging flirt with the second-best of housing and realty, giving us the subprime rout. Packaging and ordering the embodied value in hard assets and then using it to replace existing paper moneys is the challenge.

To be sure, environment and energy remain high ground interests for deciders and their public opinions, but food, water and other basics as well as healthcare, education and social security also command their attention. Creating a money which captures this value is both the goal and the only way forward for deciders who for the moment are unable to decide, due to the pitiless size of the debt and deficit crises.

Unfortunately however, time presses and accumulated wrongdoing has a heavy price. Events may therefore dictate both the pace of change, and the result, which will not at all certainly deliver the optimum choice. Ben Bernanke, more than a year ago at the 2009 Woods Hole meeting set out what he thinks (or thought) is the shibboleth, one-price-only commodity danger signal for the US economy and the US dollar: oil at $ 90 a barrel. Beyon that glass ceiling, Bernanke let it be known, he would have to think about raising interest rates. Today, Bernanke can ask Nymex, ICE or Tocom operators, or try the CFTC for ideas not on if, but when his Rubicon price could be crossed. In fact we are back to the 2007-2008 sequence, where there is no limit for hard asset price growth as long as economic growth stays strong in the East, and does not die on stage in full public view, in the West. Curiously, demand for dollars to pay for oil, rubber and rare earth elements will be so strong that it may itself slow the depreciation of the greenback, we can hope for Bernanke.

Announcing the new world reserve currency, and how it is linked to hard assets could therefore be the Black Swan surprise that everybody said would come anytime except soon which is coded language for "never". Taking the presently depreciated but Cinderella stalwart worry of trade deficits, for example, the glow of satisfaction at seeing US export numbers grow but only in direct proportion to US dollar devaluation, will rapidly pale as the J-curve and higher oil prices run riot with import numbers, and the deficit grows, and grows. Despite the grotesquely overvalued euro, this will also happen in Europe except perhaps in Germany.

With oil prices at let us say $100-plus and the other commodities at related price levels, the push for a new world money can grow very strong, very fast. We can therefore look for telltale signs in G-20 and OECD secretariat announcements, IMF directors' statements, and the other traditional sources. When it comes, however, this new money will have a real resource handle and its impact on the global economy may be combination of Heaven and Hell, delivered simultaneously. The

Brave New World may not be so very far away !

By Andrew McKillop

gsoassociates.com

Project Director, GSO Consulting Associates

http://www.marketoracle.co.uk/Article24062.htmlJoin our efforts to Secure America's Borders and End Illegal Immigration by Joining ALIPAC's E-Mail Alerts network (CLICK HERE)

Reply With Quote

Reply With Quote

Here We Go Again: Hundreds of Illegals Storm Border Fence in El...

04-18-2024, 12:26 PM in illegal immigration News Stories & Reports