Results 1 to 4 of 4

Thread Information

Users Browsing this Thread

There are currently 1 users browsing this thread. (0 members and 1 guests)

LinkBack URL

LinkBack URL About LinkBacks

About LinkBacks-

10-26-2010, 07:23 PM #1Senior Member

- Join Date

- May 2007

- Location

- South West Florida (Behind friendly lines but still in Occupied Territory)

- Posts

- 117,696

United States Judgment Days: Nov 2, voters go to Polls

United States Judgment Days

Politics / US Politics

Oct 26, 2010 - 03:51 AM

By: Gary_North

On November 2, the voters go to the polls. On November 3, the Federal Reserve goes to the mat.

On November 2, the voters will get to judge the United States Congress. On November 3, the Federal Reserve gets to judge the Federal Reserve.

Most political commentators think the voters will turn thumbs-down on the Democrats. Most economic commentators thing the Federal Reserve will turn thumbs-down on the Federal Reserve.

November 2008 was the day of judgment for the Republicans' House majority. In October, the voters did not want the Big Bank Bailout. Congress ignored the voters and did what Hank Paulson and Ben Bernanke told them to do. The Republicans got tossed out a month later. They were in the majority, and they got blamed. The Democrats voted with the Republicans, but the Republicans were on duty, and they got hammered in November.

Meanwhile, the FED more than doubled the monetary base. The FED was panic city.

The Republicans then got two years to play spoilers. The Democrats had the votes to get the shovel-ready stimulus packages passed â larger than the Big Bank Bailout. They had the votes to get Obamacare passed. They had the votes to get the bank reform bill passed. The Republicans could vote no without fear of reprisals if these laws failed to restore the economy.

The economy is still on its back. The unemployment rate is not falling. The shovel-ready stimulus did not work. Nothing Congress has done has worked.

Nothing at the FED has worked, either.

So, the voters will gain vengeance on Democrats in Congress. But will the FED gain vengeance on the FED?

THE NOVEMBER SURPRISE

Everyone is waiting for the FED's November surprise. They are waiting for an announcement of a major new plan by the FED to print up hundreds of billions of dollars. This is "quantitative easing," also known as "Bernanke as a drunken sailor on a spree." So deeply Keynesian are the nation's financial analysts that they think this will be a great benefit to the economy.

There is much speculation â in both senses â regarding what the FED will buy. It can always buy Fannie Mae and Freddie Mac bonds. It has $1.2 trillion of these toxic assets on its books already. It can buy Treasury bonds. It can buy corporate bonds. It can buy short-term T-bills. It can buy Japanese bonds, Eurozone nations' bonds, or Chinese bonds.

What is not clear is this: Will the mere creation of fiat money change the lending decisions of the nation's commercial bankers? If they decide to increase their holdings of excess reserves at the FED, the shot in the arm will be ineffective.

This is the FED's great dilemma. If it adds greatly to the monetary base, this increased spending will not multiply through the fractional reserve process if commercial bankers decide that things are risky. Are things risky? Very.

We now have a new "gate" â foreclosuregate. The big banks have played fast and loose with the paperwork on loans and titles. It looks as though millions of home mortgages could not be successfully defended in a court of law, and even if they can be defended, the entire court system would shut down if every underwater mortgage debtor demanded to see the paperwork, which the lenders cannot supply. "I'll see you in court!" will cease to have any meaning. Hardly anyone will get into court.

Here's the problem. We have been trained to view the courts as a free resource. But when anything is free, it is rationed by standing in line. The courts cannot function, once millions of people say, "I'll see you in court."

Word is getting out that the lenders cannot prove that they possess valid title to the homes. This means that home owners cannot legally be evicted if they stop paying. They need only demand proof that the agency to which they are making payments holds title.

I wrote about this over a year ago. Now the day of reckoning is here. The escape route is becoming visible to underwater mortgage payers: "Stop paying until the lender can prove that he holds legal title." The lender must make property tax payments despite the nonpayment by home owners.

The best hope that the lenders have is the fear of foreclosure by the tax man. But if home owners pay their property taxes, this threat goes away. People can live rent-free except for paying property taxes. At some point â maybe soon â this is going to dawn on desperate, underwater debtors.

The dam looks like it is about to burst. The mainstream media are sensing that the illegally handled paperwork (digitswork) is a Huge Story, one that Americans will read about or watch on the Evening News. That means there will be added coverage. Then more people will find out.

In this psychological environment, is it likely that bankers will be ready to lend? If the answer is "no," then what good will the FED's pump priming do?

The FED can say whatever it likes. It can announce some program of currency expansion. It can dutifully explain why "this time, it's different." The investors may breathe a sigh of relief and buy something. But after the hoopla dies down, what will the bankers do with the increase in legal reserves? If the answer is "increase excess reserves," then the stimulus will have little effect in the overall economy.

At that point, the FED will be sitting a larger powder keg of legal reserves. This powder keg will attract the attention of currency speculators.

A FALLING DOLLAR

For a year, the FED has kept the monetary base stable. Nevertheless, the dollar has fallen in value internationally. There is no clear reason for this. We would think that a stable money policy would increase the international purchasing power of the dollar. It has in fact stopped domestic price inflation. The consumer price index is up only by 1% over the last 12 months. The rate of increase has fallen close to zero.

Internationally, the dollar has fallen. Domestically, the dollar has stabilized. What is going on here? The FED remains silent.

Here are my two cents' worth (declining internationally, stabilizing domestically): currency speculators look at the size of the Federal deficit and assume that the FED will be forced to buy Treasury debt eventually.

"Eventually" may begin on November 3. This is what the Establishment forecasters think is likely.

Bernanke has kept saying that the Federal Funds rate will stay low â the rate at which banks lend overnight money to each other. The FED is not keeping this rate low. It merely pretends to be keeping it low. What is keeping it low is the lack of demand for overnight money. Banks that have excess reserves at the FED do not need to borrow overnight money in order to meet their legal reserve requirements.

Let me quote the late, not great felon and former Attorney General John Mitchell: "Watch what we do, not what we say." Mitchell went to jail because someone inside the White House leaked copies of the tapes of what they had said. But Mitchell was correct. Watch what the FED does, not what it says. Then watch what commercial bankers do. They may counteract what Bernanke says he is doing and the FED actually does.

Talk is cheap. Actions count. There is way more to economic recovery than what Bernanke says and the FED does. Think "green shoots."

If, in the midst of a falling dollar internationally and stable prices domestically, the FED starts pumping, I think we can expect a falling dollar internationally. If the bankers do not lend, there will be low or no price inflation domestically. But international speculators will assess what the FED is doing and what commercial bankers are likely to do.

If they think that this new policy, if any, is likely to act as a catalyst for a recovery, they will sell the dollar. They will see that the enormous powder keg of legal reserves â the FED's monetary base â is subject to a fuse. If the FED lights this fuse with major purchases of any asset class, the bankers have the power to rip the fuse out of the powder keg. But if they decide to let it burn, there will be an explosion: M1 up, M1 multiplier up, excess reserves down. Then the era of price inflation will begin.

The FED cannot control what international currency speculators will do. If they sell the dollar, Geithner will have a problem.

The official Party Line at the Treasury is that a strong dollar is necessary. Geithner keeps saying this. He says that the yuan should be stronger, but no other currency. The dollar is the world's reserve currency. The Party Line has to be "strong dollar." The Treasury is meeting the deficit at low rates because of loans from Asian central banks. If these banks perceive that the new policy of the FED is to debase the currency, they may decide to stop buying T-bills. This is not assured, but it is a major risk.

If foreigners quit buying Treasury debt, the Treasury will have to sell its debt to Americans or to the FED. If it sells to the FED, then the crisis will escalate. The Treasury will absorb American investors' capital, and it will also be the unindicted co-conspirator of the FED.

BERNANKE'S MINE FIELD

The FED is in the crosshairs. This has never happened before. The swing voters are Tea Party people. They have heard the story of the Federal Reserve over the last two years. Bernanke is about to lead the Board of Governors across a political mine field.

The new Congress will not be ready to extend him a lot of credit. He may get some, but he will not get much. He had better be sure that any newly announced policy does not send up red flags between November 3 and January 2. A new era is coming â if not for the nation, then at least for the Federal Reserve System. Bernanke's days of wine and roses are also about to end.

The mainstream forecasters say that the FED will announce a major policy on November 3. Everyone expects an announcement of quantitative easing. But Bernanke will provide this. Yes, it is possible that the FED will begin a program of asset purchases, but Bernanke's words will be moderate and nonspecific. This man uses verbal chloroform the way that Greenspan used gibberish. If he were the head of the People's Bank of China, they would call him Lo-Kee.

If he is wise, he will tell the world that the Federal Open Market Committee will continue to monitor the situation closely. He will assure people that the Federal Funds rate will be kept close to zero percent for an indefinite future. He will say that there are signs of economic recovery, even though the rate of unemployment has remained higher than is consistent with long-term economic growth.

If he announces a major policy change, it will mean that he sees winter coming for all those green shoots. It will mean that Obama's stimulus has failed, that the shovels were not ready, and the FED's previous policies were insufficient to produce the promised economic recovery. Any major policy change will be a public announcement of failed programs, both by Congress and the FED.

If he says that it is time for a major policy change, this will be seen as a "Hail, Mary" pass. That is what quarterbacks use in the final minutes of a game in which the score is 13 to 7 against them. Bernanke threw one in late 2008: the more than doubling of the monetary base. But he said nothing. He was mute in September and October of 2009. Paulson did all the talking. When Bernanke bothered to show up, he was Paulson's potted plant.

If he makes a statement of a major change of policy, and then describes this policy, this will be the first time in his career at the FED in which he did either. This man hides behind a Maginot Line of footnotes in order to avoid committing to anything, other than maintaining the FedFunds rate close to zero percent, which the FED does not actually do.

If he says anything big, this will send a signal to international currency speculators: "Gentlemen, start your engines. Sell the dollar short."

Why would he do this? Why would he risk making a major announcement on the day after the elections?

This country will be facing two years of political gridlock. The Republicans will start holding hearings on anything the White House has done that will get air time. The drip-drip-drip of subpoenas will begin in January, and they will not stop.

Why would an announcement from Bernanke that he and his colleagues will begin a program mass inflation win him support in Congress? If he does this, he is dumber than a Dave Barry comparison of dumbness. He will give the new Republican majority in the House two months to prepare their questions for him.

The boiling economic issue today is the mortgage market and the banks. If he thinks that what the Congressional Republicans are waiting for is a policy of mass inflation, then his political instincts are even worse than his Keynesian tool kit, which is saying something.

Right now, he is safe. The mortgage fraud issue is not perceived as his fault. He came into office in February 2006. By that time, the housing bubble had begun to peak. No one has blamed him for Greenspan's bubble. He has been given a free pass. He needed it.

If he announces a policy of quantitative easing on the day after the elections, he will face a boiling pot of tea poured into his lap. Paul Krugman will applaud on November 4, but how many votes will Krugman have in the House on January 2?

CONCLUSION

If Bernanke announces a new policy of quantitative easing on November 3, he will light the fuse. It is a monetary fuse. It is also a political fuse.

What's in it for him, other than grief?

If he does this, he had better offer a clear statement â from Bernanke? â about exactly why the FED's policies have failed for two years, and why the new policy will get those green shoots growing. Otherwise, he will not be walking into a mine field; he will be running into it.

http://www.marketoracle.co.uk/Article23772.htmlJoin our efforts to Secure America's Borders and End Illegal Immigration by Joining ALIPAC's E-Mail Alerts network (CLICK HERE)

-

10-26-2010, 08:05 PM #2Senior Member

- Join Date

- May 2007

- Location

- South West Florida (Behind friendly lines but still in Occupied Territory)

- Posts

- 117,696

Bernanke's $4 Trillion Quantitative Easing Dilemma

Interest-Rates / Quantitative Easing

Oct 26, 2010 - 10:16 AM

By: Mike_Whitney

Ben Bernanke is in a real fix. His quantitative easing (QE) program is designed to boost stock prices, lower bond yields, and weaken the dollar.

But the market has already priced all that in, so when he announces the start of the program on November 3, there's a good chance that things will either stay the same or head in the opposite direction. That's bad for Bernanke. Just imagine if the dollar strengthens just as the Fed chairman begins buying-up Treasuries to push the dollar down. He'll look pretty foolish. But that could happen because the dollar has already slipped nearly 7% since August and is overdue for a rebound.

So, what should he do? Should he go ahead and launch his program anyway knowing it could backfire and further damage his credibility or scrap the whole deal and move on to Plan B?

The truth is, he has no choice. If he doesn't follow through now, investors will accuse him of "withdrawing liquidity" and send the market into a nosedive. So, he has to go forward and let the chips fall where they may. If QE2 turns out to be a bust, so be it.

A new report from Goldman Sach's economist Jan Hatzius figures that "the Fed will need to print $4 trillion...to close the Taylor gap." (zero hedge) That means it will take roughly $4 trillion for QE to do what it's supposed to do. New York Times columnist Paul Krugman's estimates are even higher. He thinks it will take $8 to 10 trillion of QE to push down long-term rates enough to sustain the recovery. Of course, no one is even considering expanding the Fed's balance sheet by that amount because it would put the central bank's future at risk and might not work anyway. Instead, Bernanke plans to take baby steps, purchasing $200 to $300 billion in Treasuries at a time, hoping that the smaller amounts buoy stocks and increase investment in the real economy. In other words, QE2 is not a really serious commitment of resources to address deflationary pressures, excess capacity or high unemployment at all. It's more like giving aspirin to a cancer patient. There may some temporary relief, but the overall effects will be negligible.

That's not to say that the Fed isn't a powerful institution. It is. The Fed controls short-term interest rates and short-term rates can either stimulate growth or send the economy into a tailspin. They can guide the economy to years of productivity and prosperity or generate gigantic speculative bubbles that end in disaster. But, in a liquidity trap--when interest rates are stuck at zeroâmonetary policy is largely ineffective so the Fed is dead-in-the-water. It doesn't matter how cheap money is when people aren't borrowing. And, people aren't borrowing because they're broke. The Fed doesn't have the ability to change that. Bernanke may wish he was "Helicopter Ben" and could drop bundles of greenbacks over America, but the truth is, only congress has that power and they're not taking advantage of it. They're more worried about deficits.

So, QE won't succeed because it doesn't address the real issue, which is demand. In theory, when the Fed buys bonds, it pushes investors into riskier assets, like stocks. That, in turn, inflates equities prices which (supposedly) triggers additional hiring and lowers unemployment. It's a persuasive theory, but it won't work. Here's an excerpt from an article in the Wall Street Journal which explains why:

"While more quantitative easing will help to keep interest rates low, primary dealer banks aren't fully convinced that the move will prove to be the U.S. economy's knight in shining armor.

"It may help to lower rates temporarily," said Ward McCarthy, chief financial economist and managing director of the fixed-income division at Jefferies & Co. in New York, "but is unlikely to have a significant beneficial effect on the economy."

That is because such a program won't ease credit conditions for small businesses that are dependent on banks for lending, he said, nor will it lower borrowing costs for homeowners who are unable to refinance their mortgages because home prices have fallen." (No Fix in Quantitative Easing, Deborah Lynn Blumberg, Wall Street Journal)

So, if QE doesn't help small businesses (which create most of the country's new jobs) or homeowners, than how can it lower unemployment, trim excess capacity, or increase aggregate demand? It can't. At best, it will merely boost asset prices and create more bank reserves while the real economy continues to languish in a near-Depression.

Naturally, the prospect of the Fed adding trillions of dollars to the money supply has trading partners in a panic forcing some to regulate capital inflows and prepare for a savage round of competitive devaluation. At this weekend's meeting of the G-20 in Gyeongju, South Korea, German finance minister, Rainer Brüderle lashed out at the Fed's QE program saying, âExcessive, permanent money creation in my opinion is an indirect manipulation of an exchange rate.âJoin our efforts to Secure America's Borders and End Illegal Immigration by Joining ALIPAC's E-Mail Alerts network (CLICK HERE)

-

10-26-2010, 08:11 PM #3Senior Member

- Join Date

- May 2007

- Location

- South West Florida (Behind friendly lines but still in Occupied Territory)

- Posts

- 117,696

Quantitative Easing (QE2): Who Gets the Fedâs Printed Money?

Interest-Rates / Quantitative Easing

Oct 26, 2010 - 08:49 AM

By: Chris_Ciovacco

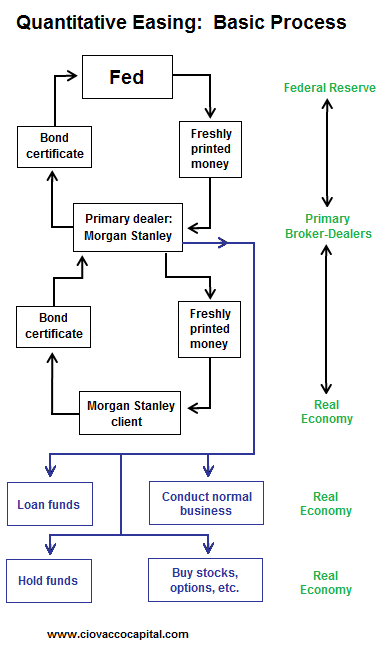

Part 2 of a 6 Part Video Series on Quantitative Easing: In Part 1: Quantitative Easing Targets Asset Prices, Not Bank Reserves, we discussed how Mr. Bernankeâs quantitative easing program is implemented via the Fedâs eighteen primary dealers, not traditional banks.

We do not know the size of the Fedâs program, nor do we know how the markets will react in the short-term. However, one thing we know with near certainty â a large quantity of newly printed money is going to flow from the Fed to the eighteen primary dealers. We also know a significant amount of the electronic greenbacks will flow from the primary dealers into the accounts of their clients.

Since the Fed encourages the primary dealers to offer client bonds in the QE competitive bidding process, it is helpful for investors to know more about the clients of the primary bond dealers. Sovereign wealth funds, who do business with numerous primary dealers, will be one of the most influential groups who may participate in QE2. A sovereign wealth fund is a state-owned investment fund, which holds a wide variety of financial assets, including stocks, bonds, commodities, currencies, precious metals, and real estate.

One of the largest sovereign wealth funds is the Norway Global Government Pension Fund, which holds somewhere in the neighborhood of $400 billion in assets. Others include the China Investment Corporation ($300 billion), Singapore Investment Corporation ($250 billion), Hong Kong Monetary Authority ($225 billion), the Russia National Welfare Fund ($140 billion), and the Australian Future Fund ($60 billion).

Video: http://www.youtube.com/watch?v=voMm_6tb ... r_embedded

To give a hypothetical example of how the Fedâs newly printed money can make its way around the globe, assume the following: (a) concerned about the currency risk associated with holding too many U.S. Treasuries, the Singapore Investment Corporation (SIC) decides to sell some bonds to the Fed via the QE2 program, (b) the Fed takes the Treasuries and the SIC gets newly printed U.S. dollars in return, (c) since holding U.S. dollars also entails currency risk, the SIC decides to diversify into gold, global stocks, and emerging market bonds. This hypothetical example shows how the Fedâs printing press can, in theory, create demand for other assets and thus, help drive asset prices higher. Higher asset prices can help improve strained balanced sheets which can, in theory, spark more spending, investing, borrowing, and hiring (emphasis on in theory).

Understanding the global footprints of the primary dealers and their clients allows us to visualize the broad geographic reach of the Fedâs printing press. Understanding the buying power and investment influence of large clients of the primary dealers, like sovereign funds, helps us understand how QE2 may potentially impact a wide range of markets from currencies to commodities.

The flow chart below shows how the Fedâs newly printed cash can flow from the Fed to the primary dealer, then to the primary dealerâs clients.

With the million dollar question relative to QE2 being the magnitude of the Fedâs planned bond purchases, we can expect some volatile trading sessions for the next week or so. According to a Forbes/CNN article:

Economists at Goldman Sachs estimate the Federal Reserve may need to buy a staggering $4 trillion worth of assets such as Treasury securities to get the economy rolling again. The Goldman economists, Jan Hatzius and Sven Jari Stehn, donât expect the Federal Reserve to go nearly that far when it resumes its asset-purchasing quantitative easing policy. Citing many officialsâ unease with the prospect of adding significantly to the Fedâs already bloated balance sheet, Goldman expects the Fed to end up buying around $2 trillion worth of assets over the next few years.

Traders, money managers, and active investors may want to get some extra rest this weekend; with mid-terms and a Fed announcement coming early next week, both stress levels and market volatility will most likely be elevated.

By Chris Ciovacco

Ciovacco Capital Management

http://www.marketoracle.co.uk/Article23785.htmlJoin our efforts to Secure America's Borders and End Illegal Immigration by Joining ALIPAC's E-Mail Alerts network (CLICK HERE)

-

10-26-2010, 08:14 PM #4Senior Member

- Join Date

- May 2007

- Location

- South West Florida (Behind friendly lines but still in Occupied Territory)

- Posts

- 117,696

Quantitative Easing Targets Asset Prices, Not Bank Reserves

Stock-Markets / Quantitative Easing

Oct 26, 2010 - 08:43 AM

By: Chris_Ciovacco

With markets coming off of overbought levels, bullish sentiment high, and gold backing off a vertical ascent, we believe investors need to be ready for a quantitative easing (QE) disappointment pullback. A âbuy the QE rumor, sell the QE newsâJoin our efforts to Secure America's Borders and End Illegal Immigration by Joining ALIPAC's E-Mail Alerts network (CLICK HERE)

Reply With Quote

Reply With Quote

Catholic bishops urge Congress to spend $20 BILLION on programs...

05-14-2024, 09:45 AM in General Discussion