Results 1 to 3 of 3

Thread Information

Users Browsing this Thread

There are currently 1 users browsing this thread. (0 members and 1 guests)

LinkBack URL

LinkBack URL About LinkBacks

About LinkBacksThreaded View

-

11-03-2011, 12:10 AM #1Senior Member

- Join Date

- May 2007

- Location

- South West Florida (Behind friendly lines but still in Occupied Territory)

- Posts

- 117,696

Day of reckoning for shadow inventory & distressed prope

Day of reckoning for shadow inventory and distressed properties â 40 percent of properties in foreclosure have not made a payment in two years or more.

2 Nov, 2011

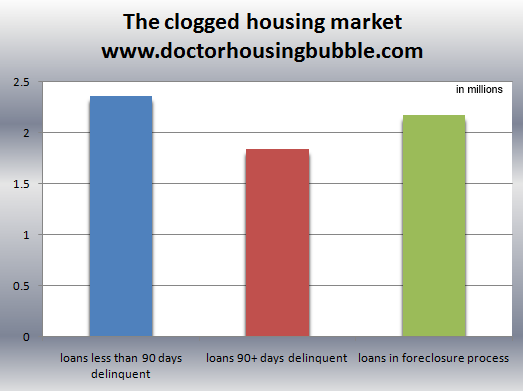

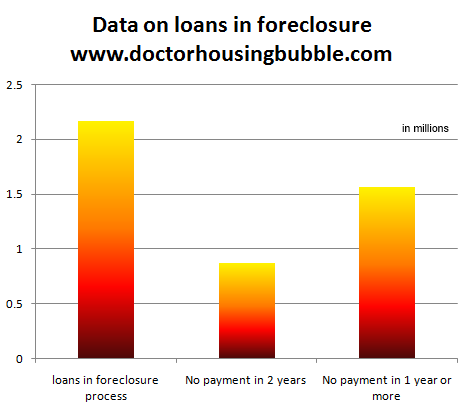

What we are witnessing on a large scale is an economy that has it completely backwards when it comes to banking and housing. Homes and the financial grease that keep the system running should be an extrapolation of an underlying healthy employment market. Today we have a misfit system of denial, outright corruption, and graft that is largely making our banking system unrecognizable. It is astounding to see how many people simply assume that the distressed pipeline has somehow miraculously disappeared. It emphatically has not. Data released this week shows that 2.17 million loans are actively in foreclosure. Of these loans, 40 percent have not made a payment in over two years! 72 percent have not made a payment in over one year! In essence, just like with our financial fixes, this has been the equivalent of covering up our eyes like a child fearing the boogieman and pretending there was no issue in the system. Psychologically you have many that bought in bubble markets the last few years trying to convince each other that they somehow made a wise decision simply because they did not purchase at the peak. The data on the clogged toilet of housing distressed properties shows us that we still have some serious plumbing problems ahead.

The pipeline of distressed properties sits at 6.37 million

Given the dismal re-default rates and cure opportunities most loans that get behind will end up as lower priced sales either through a short sale or a full-fledged foreclosure. It might help to get a full snapshot of the current situation:

In all some 6.37 million homes can be considered distressed. This is a large pipeline. Given the astounding reality that over 40 percent of the loans in foreclosure have made no payment in two years, you can understand why the other two columns are brimming to the top. When we splinter out the foreclosure column the data looks daunting:

Not much has improved on this front largely because the economy is still mired in an economic mess and Europe is dealing with what else, a giant debt crisis. We are inextricability linked to global banking markets and our entire financial edifice rests on debt. Not just a little bit of debt but heaping amounts of debt. The game can only go on for as long as you can convince enough suckers to jump into the system to believe that the next decade will follow similar patterns to those that they know in the 1970s, 1980s, 1990s, or 2000s. You can rest assured that the upcoming decade will not resemble any of those.

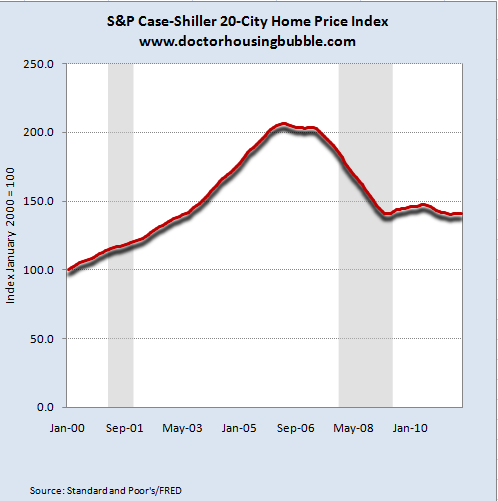

The name of the game is confidence. The housing bubble was largely a giant psychological ploy based on easy access to debt and a large cult like mentality that home values would only go up irrespective of underlying economic fundamentals. Bubbles work this way and play on consumer behavior and the flaws of our primordial brains. Deep down we still have a few things to work out and we are seeing these things play out on a global stage. Around the world you are seeing housing bubbles from Australia to China to the United States. Prices have done very little in the last four years after collapsing:

Those that make the case for diving in right now usually have simplistic visions of the new financial system. The dynamics of the current system move much faster and some are using outdated models and assuming the demographics of yesterday will apply to the future. These people even miss simple benefits of renting; like the flexibility offered especially for younger professional couples who need to move around and with careers shifting so quickly, many may end up in New York, Chicago, Los Angeles, or any other large city. Renting provides quick mobility. Buy now and you can expect to stay put for a very long time. Iâve talked with a few younger and bright professional couples and some are actually very happy to talk about renting. Even four years ago this was rare to hear. Today the oneâs arguing for buying in this market may largely be justifying their purchase and assuming some kind of Mad Men era of prosperity.

A quick glance on Realtor.com shows that roughly 4.3 million properties are up for sale nationwide:

The clogged housing pipeline is up over 6.37 million! I find this comparison interesting because much of the distressed pipeline is behind the scenes. Take California as an example:

Non-distressed for sale: 169,000

Notice of default: 85,000

Scheduled for auction: 55,000

Bank owned homes: 64,000

The bank owned category is large at 64,000 but more troubling is you have 55,000 properties scheduled for auction that are likely to be inventory shortly (even after delaying the inevitable for years). What will this do to prices? Push them lower:

CA median price

September 2010: $265,000

September 2011: $249,000

Keep in mind the above price decline has occurred from a peak median price drop from $484,000 in 2007. Maybe the 22+ percent underemployment rate has something to do with it or the fact that with lower wages, more money is being floated to housing and taking away from the productive side of the economy. Ironically some of the best boom times for the nation occurred when home prices were moderately priced and people didnât need maximum leverage to squeeze into the party dress house to think they looked good.

It is interesting to hear some people have a âI got mine so screw you attitudeâJoin our efforts to Secure America's Borders and End Illegal Immigration by Joining ALIPAC's E-Mail Alerts network (CLICK HERE)

Reply With Quote

Reply With Quote

DHS says 'privacy' of migrants on terrorist watchlist is greater...

05-17-2024, 09:42 PM in illegal immigration News Stories & Reports