Results 1 to 2 of 2

Thread Information

Users Browsing this Thread

There are currently 1 users browsing this thread. (0 members and 1 guests)

LinkBack URL

LinkBack URL About LinkBacks

About LinkBacksHybrid View

-

11-20-2011, 10:25 PM #1Senior Member

- Join Date

- May 2007

- Location

- South West Florida (Behind friendly lines but still in Occupied Territory)

- Posts

- 117,696

EU Bank Run Downward Spiral, Goldman Final Phase World Domin

The European Bank Run Downward Spiral, Final Phase Of Goldmanâs World Domination Plan

Interest-Rates / Global Debt CrisisNov 20, 2011 - 10:39 AM

By: PhilStockWorld

Courtesy of ZeroHedge. View original post here. Submitted by Tyler Durden. http://tinyurl.com/7gfo2o8

"Nervous investors around the globe are accelerating their exit from the debt of European governments and banks, increasing the risk of a credit squeeze that could set off a downward spiral. Financial institutions are dumping their vast holdings of European government debt and spurning new bond issues by countries like Spain and Italy. And many have decided not to renew short-term loans to European banks, which are needed to finance day-to-day operations. "

So begins an article not in some hyperventilating fringe blog, but a cover article in the venerable New York Times titled "Europe Fears a Credit Squeeze as Investors Sell Bond Holdings." Said otherwise, Europeâs continental bank run in which virtually, but not quite, all banks are dumping any peripheral exposure with reckless abandon is now on. Granted, considering the epic collapse in bond prices of Italian, French, Austrian, Hungarian, Spanish and Belgian bonds which all hit record wide yields and spreads in the past week, and furthermore following last weekâs "Sold To You": European Banks Quietly Dumping â¬300 Billion In Italian Debt" http://www.zerohedge.com/news/sold-you- ... alian-debt which predicted precisely this outcome, the news is not much of a surprise. However, learning that everyone (with two exceptions) has given up on Europeâs financial system should send a shudder through the back of everyone who still is capable of independent thought â because said otherwise, the worldâs largest economic block is becoming unglued, and its entire financial system is on the edge of a complete meltdown. And just to make sure that various fringe bloggers who warned this would happen over a year ago no longer lead to the hyperventilation of the venerable NYT, below, with the help of Goldmanâs Jernej Omahan, we bring to our readers the complete annotated and abbreviated beginnerâs guide to the pan-European bank run.

But first some more details from the NYT: http://www.nytimes.com/2011/11/19/busin ... ted=2&_r=1

The flight from European sovereign debt and banks has spanned the globe. European institutions like the Royal Bank of Scotland and pension funds in the Netherlands have been heavy sellers in recent days. And earlier this month, Kokusai Asset Management in Japan unloaded nearly $1 billion in Italian debt.

At the same time, American institutions are pulling back on loans to even the sturdiest banks in Europe. When a $300 million certificate of deposit held by Vanguardâs $114 billion Prime Money Market Fund from Rabobank in the Netherlands came due on Nov. 9, Vanguard decided to let the loan expire and move the money out of Europe. Rabobank enjoys a AAA-credit rating and is considered one of the strongest banks in the world.

American money market funds, long a key supplier of dollars to European banks through short-term loans, have also become nervous. Fund managers have cut their holdings of notes issued by euro zone banks by $261 billion from around its peak in May, a 54 percent drop, according to JPMorgan Chase research.

Is this setting familiar to anyone? It should be: "Experts say the cycle of anxiety, forced selling and surging borrowing costs is reminiscent of the months before the collapse of Lehman Brothers in 2008, when worries about subprime mortgages in the United States metastasized into a global market crisis."

Ah, but there is one major difference: last time around, the banks were not all in on the wrong side of the worldâs worst poker hand (as described by Kyle Bass earlier). Now they are. And should Europeâs banks begin a domino-like spiral of collapse, there will be nobody to bail out first Europe, then Japan, then China, then the US and finally the world.

But lest someone suggest this is merely the deranged ramblings of yet another blogger, here is Goldman Sachs with a far more cool, calm and collected explanation for why we should all panic (which comes at the sublime moment: just as Goldman takes over all the key political locus points of the European continent: more on that in the conclusionâ¦)

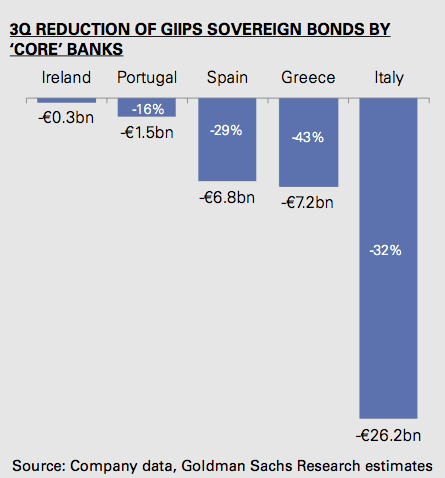

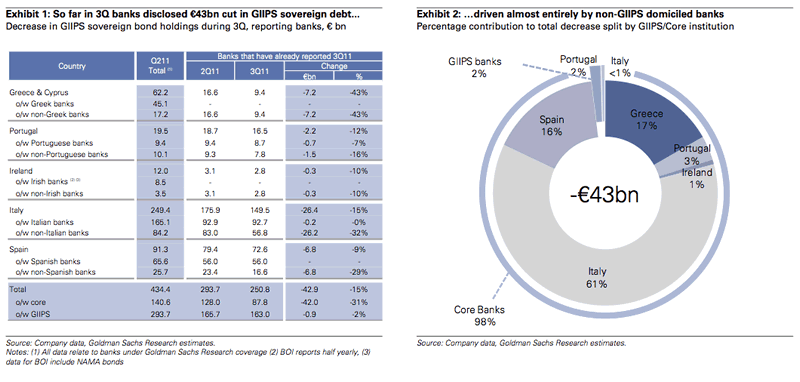

Coreâ banks cut GIIPS debt by â¬42 bn (-31%) in 3Q; a manifestation of PSI side-effects?

In 3Q2011, banks from the âcoreâ cut their net GIIPS sovereign debt holdings by â¬42 bn (or by one-third), mostly Italian (â¬26 bn), Spanish (â¬7 bn) and Greek (markdown of â¬7 bn). French and Benelux banks cut their exposures most, by â¬21 bn and â¬9 bn, respectively. GIIPS portfolios remained unchanged with periphery banks.

Greek PSI sets a risky precedent, in our view, as the prospect of âvoluntaryâ haircuts becoming a template for GIIPS crisis resolution could drive exposure reduction. Core banks now have â¬88 bn of GIIPS sovereign bonds remaining. We expect this to decline. Problematically, we observe that GIIPS bond reductions are not resulting in âcoreâ bond purchases but in a rise in deposits at the ECB.

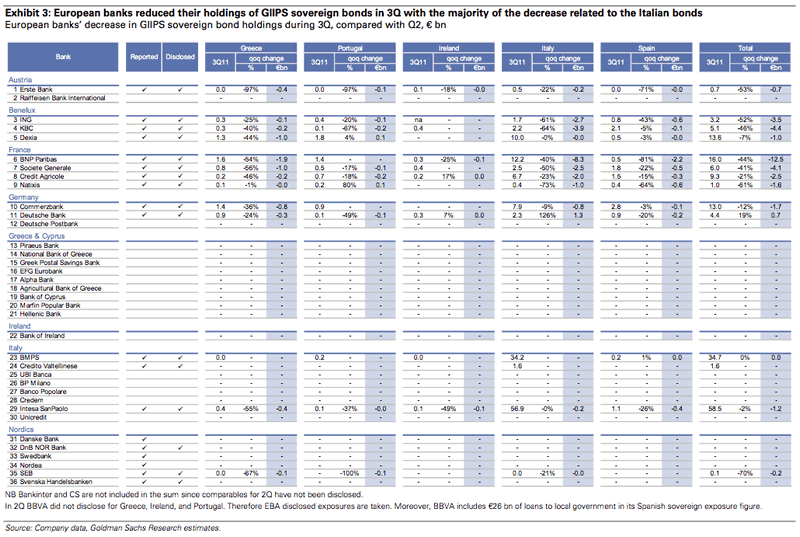

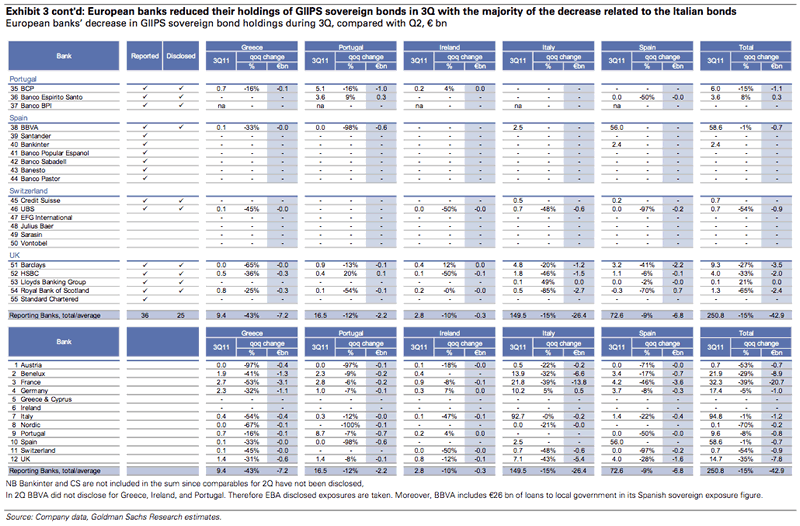

The disposal of GIIPS sovereign debt accelerated during 3Q2011, and we highlight the following.

Banks cut net GIIPS sovereign exposure by â¬43 bn. The largest reductions relate to Italian (â¬26 bn), Spanish (â¬7 bn) and Greek (â¬7 bn) net sovereign debt positions.

Almost all of the reduction (â¬42 bn) came from banks in the European âcoreâ, where the GIIPS bond positions therefore fell by just over one-third (31%). At the same time the banks from the âperipheryâ kept their exposures unchanged.

French (â¬21 bn) and Benelux (â¬9 bn) banks reduced their exposure most.

Individually BNP (â¬12 bn), KBC (â¬4.4 bn), SG (â¬4.1 bn), BARC (â¬3.5 bn) and ING (â¬3.5 bn) cut the net sovereign exposures most, in absolute terms.

We expect this trend to extend into 4Q and to ultimately lead to a long-term reduction GIIPS bond holdings by core banks.

Greek PSI â and the âvoluntaryâ 50% haircut â has changed the risk perception of GIIPS bonds. We believe it has allowed for an assumption that PSI will be used as a template in helping other GIIPS sovereigns improve their public finances. Such intention is denied by policy makers. Banks, on the other hand, express their view of the likelihood of such an event through the changes in their net positions.

It is important to emphasizes that a bankâs decision to hold sovereign debt is not an expression of an investment preference. Rather, it is a decision related to liquidity management. As such banks seek ârisk freeâ assets that can be used to access liquidity at any time, particularly at the time of crisis. Regulators continue to treat sovereign debt as highest-quality and risk free (0% risk-weight) collateral. With no RWA constraint and full refinancing eligibility, banks are encouraged to hold sovereign debt; its (selective) transition from a ârisk freeâ to a âriskâ asset is therefore unexpected and highly damaging.

Earlier we said all but two entities have been dumping PIIGS (or GIIPS as Goldman prefers to call them). Sure enough, one of the unlucky two tasked with buying everything sold in the secondary market is of course the ECB: the same bank that everyone is accusing of not doing more to help.

Funding: Increasingly reliant on the ECB

The use of ECB facilities rose again in October, driven by Spanish (â¬7 bn) and Italian (â¬6 bn) banks. For 4Q, we expect a sharp increase in use by Italian banks, driven by: (1) LCHâs increased margin requirements on Italian REPOs, which now make market REPOs comparatively more expensive than those at the ECB; and (2) a steady fading of the ECB funding âstigmaâ. It is possible that the majority of the â¬300 bn of interbank funding and market REPOs could end up on ECBâs balance sheet. That alone would have the capacity to lift current ECB use from â¬579 bn to just below â¬900 bn. This level of use would compare with previous crisis peak levels (2009) of â¬870-897 bn.

We have long argued that the ECB has capacity to back-stop bank funding requirements â and there is no change to this view. That said, a gradual closing of the last functioning wholesale funding market â short-term REPOs, backed by government bonds â is certainly not an encouraging sign. The re-opening of the long-term funding markets has been pushed further out, in our view.

LCH triggers increased margin requirements on Italian REPOs

On November 9, 2011, LCH.Clearnet (LCH) announced its decision to increase âdeposit factorsâ applied to Italian debt repo transactions (e.g. haircut on collateral) by 3.5% to 5% depending on the duration of the collateral. The move was not a surprise as LCHâs Risk Management Framework states that it âwould generally consider a spread of 450bp over the 10-year AAA benchmark to be indicative of additional sovereign riskâJoin our efforts to Secure America's Borders and End Illegal Immigration by Joining ALIPAC's E-Mail Alerts network (CLICK HERE)

Reply With Quote

Reply With Quote

Migrants Breach Fortified Border Barrier, March Through Texas...

05-16-2024, 08:20 PM in illegal immigration News Stories & Reports