Results 1 to 1 of 1

Thread: Gold Rises as the Euro Vaporizes

Thread Information

Users Browsing this Thread

There are currently 1 users browsing this thread. (0 members and 1 guests)

LinkBack URL

LinkBack URL About LinkBacks

About LinkBacks-

05-14-2010, 05:40 PM #1Senior Member

- Join Date

- May 2007

- Location

- South West Florida (Behind friendly lines but still in Occupied Territory)

- Posts

- 117,696

Gold Rises as the Euro Vaporizes

Gold Rises as the Euro Vaporizes

Currencies / Euro

May 14, 2010 - 11:07 AM

By: Andy_Sutton

This wasn’t supposed to happen. When it was introduced 11 years ago, the Euro was to be the world’s newest, biggest, and best yet currency. There were strict guidelines for getting into Club Euro and you’d better follow them if you didn’t want to be voted off the island. What became immediately clear is that there were stronger members and weaker members. That fact is becoming increasingly apparent as the real state of the Eurozone now comes into clear focus. Over the years, rules were bent, concessions made, and explanations given, all for the purposes of justifying short-term benefits such as the availability of Italian milk to the Club. Yes, Italian milk.

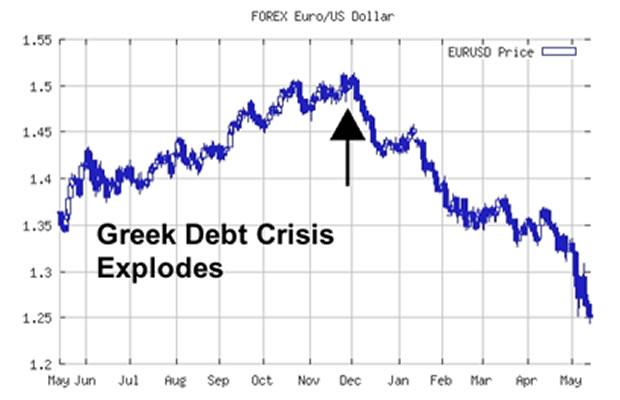

In yet another example of the failure of globalization, or regionalization as it were, the Euro is poised on the precipice of disintegration. Ironically, it will not be the overprinting and resultant hyperinflationary spiral that kills the Euro, but dead weight in the form of various Eurozone welfare states. Germany and some of the other quasi-responsible members simply cannot carry their own burdens and those of Greece, Spain et al. The $1 Trillion rescue fund created in haste this past weekend was intended to inspire confidence in the dying behemoth. Instead, the sheer magnitude of the bailout has done the exact opposite.

The Euro-Dollar pair has now sunk below pre-bailout levels and there is a good deal of doubt as to whether rescue recipients will be willing or able to hold up their end of the bargain. I pointed this out in last week’s piece. The temporary euphoria created by a trillion dollars of palliative paper is already gone. This is something that was alluded to in these pages years ago; the law of diminishing returns applies to stimulus and bailouts. As the periods of crisis occur in a more frequent fashion, the effectiveness of Keynesian monetary policy falls commensurately.

That aside, there are several other points that must be addressed as we examine the latest Tower of Babel in the global macroeconomic arena.

National Sovereignty Ceded

While anyone looking at the debt picture could tell that Greece (like so many others) was in trouble almost since its acceptance into the Eurozone, its problems burst into the international media in early 2010. One of the first things that many people noted was the major difference between the Greek government and that of America. Greece was hamstrung in that it did not have its own national bank; it relied on the ECB. While I am not a fan of national or central banks absent a strict Gold standard, this total absence of flexibility accelerated the Greek crisis in months, rather than years. Greece had given up its national identity to join the Club. And for a time it worked. The people of Greece enjoyed lavish social benefits and a carefree lifestyle. As an IMF official recently said, however, and I am paraphrasing: “The party is over�Join our efforts to Secure America's Borders and End Illegal Immigration by Joining ALIPAC's E-Mail Alerts network (CLICK HERE)

Reply With Quote

Reply With Quote

72 Hours Till Deadline: Durbin moves on Amnesty

04-28-2024, 02:18 PM in illegal immigration Announcements