Results 1 to 1 of 1

Thread Information

Users Browsing this Thread

There are currently 1 users browsing this thread. (0 members and 1 guests)

LinkBack URL

LinkBack URL About LinkBacks

About LinkBacks-

10-30-2010, 09:13 PM #1Senior Member

- Join Date

- May 2007

- Location

- South West Florida (Behind friendly lines but still in Occupied Territory)

- Posts

- 117,696

Double Dip Recession Delayed, Not Derailed

Double Dip Recession Delayed, Not Derailed

Economics / Double Dip Recession

Oct 30, 2010 - 07:29 AM

By: Mike_Shedlock

The BEA Advance GDP for Third Quarter 2010 came in at +2.0%. However, Table 2. Contributions to Percent Change in Real Gross Domestic Product shows that Change in private inventories contributed +1.44 while real final sales contributed a mere .6.

How sustainable is that?

The answer is not very. This is likely the last hurrah for inventory replenishment even without factoring in upcoming cutbacks at the state level.

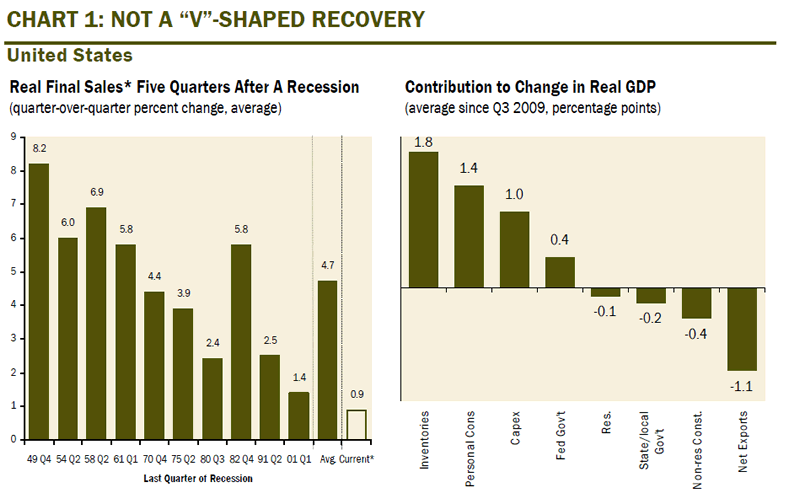

Not a V-Shaped Recovery

In terms of real final sales, this "recovery", is the weakest on record. Dave Rosenberg has some thoughts on that in Lunch with Dave. https://ems.gluskinsheff.net/Articles/L ... 102910.pdf

U.S. REAL FINAL SALES 60 BASIS POINTS SHY OF DOUBLE-DIPPING

The major problem in the third quarter report was the split between inventories and real final sales. Nonfarm business inventories soared to a $115.5 billion at an annual rate from the already strong $68.8 billion build in the second quarter â this alone contributed 70% to the headline growth rate last quarter. If we do get a slowdown in inventory investment in Q4, as we anticipate, it would really not take much to get GDP into negative terrain. We estimate that if the change in inventories slowed to about $94.0 billion in Q4 (about $22 billion below Q3 levels), GDP would contract fractionally. In other words, it wonât take much for GDP to slip into negative terrain.

The recession may have technically ended, but outside of inventories, and the best days of the re-stocking process look to be behind us, this has been a listless recovery. At 60 basis points above zero, real final sales are just a shock away from double-dipping â a shock like looming tax hikes, accelerating fiscal cutbacks at the state/local government level or the millions of â99ersâJoin our efforts to Secure America's Borders and End Illegal Immigration by Joining ALIPAC's E-Mail Alerts network (CLICK HERE)

Reply With Quote

Reply With Quote

Americans Want Congress to Act on Border Security. Will They?

05-04-2024, 10:39 AM in illegal immigration News Stories & Reports