Results 11 to 20 of 20

22Likes

22LikesThread Information

Users Browsing this Thread

There are currently 1 users browsing this thread. (0 members and 1 guests)

LinkBack URL

LinkBack URL About LinkBacks

About LinkBacks-

08-11-2017, 09:07 AM #11Super Moderator

- Join Date

- May 2005

- Location

- Heart of Dixie

- Posts

- 36,012

Tuesday, September 23, 2008

Illegal Immigration and the Subprime Mortgage Crisis

With all the blame being passed back and forth, one of the key causes of the current financial crisis is being ignored by both parties and the mainstream media - illegal immigration.

From a Reuters article dated Jan 30, 2008:

As an economic slowdown and the subprime mortgage crisis deepen across the United States, Hispanic immigrants are increasingly in danger of losing their jobs and their homes.USAToday reports that minorities are hit especially hard by the subprime scandal:

Illegal immigrants were able to buy U.S. homes during the boom years, either by showing evidence that they pay taxes or by simply presenting false documents.

Many of them took out high interest fixed-rate loans or subprime mortgages with a low entry rate that later rose sharply.

Recent immigrants lack credit histories, and 35% of Latino families don't have checking accounts. Hispanic families are more apt to have undocumented income, leading them to lenders who make loans without income verification, according to the National Council of La Raza.

The article goes on to blame politicians and community organizers for pressing for more minority home ownership:

Another reason for the subprime surge: Lenders have been supported by politicians and community leaders eager to promote minority homeownership, which remains about 25 percentage points below that of white non-Hispanics.The West Australian reports 'NINJA' loans were the cause of the world-wide financial meltdown:

"Access became such a buzzword that people forgot about basic lending practices," says Keith Corbett, executive vice president of the Center for Responsible Lending. "You are really in debt servitude, having a loan with a loan-to-value ratio of 100% or greater."

Perhaps we should have known it was too good to be true when an American lender came up with the ninja loan. No, its not a loan draped in black that flies across the rooftops of the Imperial Palace. It is a loan offered to potential homebuyers who have No Income, No Job, No Assets.

[W]hen banks and non-banks, particularly those in the US, ran out of risk-free clients they moved on to riskier and riskier customers. Hence, the ninja loan, the sub-prime mess and the turmoil we have today.

The target customer for 'NINJA' loans is the illegal immigrant, because they are the ones who have no verifiable income, no verifiable employment, and no social security number with which to track credit worthiness. Since we have no way of tracking the credit history of illegal immigrants, they are capable of just walking away from their loans as soon as their adjustable rates went up.

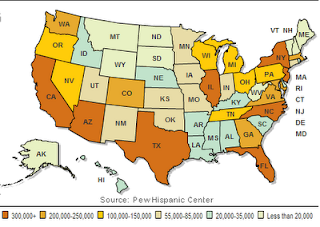

As such, the greatest amount of foreclosures occur in states that are also suffering the greatest amount of illegal immigration, as depicted in these two charts:

Illegal immigrant populations by state:

Source: Pew Hispanic Center

Home Mortgage Foreclosures by state:

Source: RealtyTrac

There are those that place the blame for these risky 'NINJA' loans on the lenders that made them available to those who clearly had no means of paying them back, but these people fail to recognize the role the Community Reinvestment Act played.

The Community Reinvestment Act, which requires lenders to make loans available throughout their entire market and not just in wealthier neighborhoods, was modified by the Clinton administration to require lenders to make these unsustainable loans available inorder to reach certain percentage of minority home loan goals.

In 2003, the Bush adminisatration along with Sen. John McCain recognized that the two largest, quasi-governmental organizations that were garruanteeing these risky loans, Fannie Mae and Freddie Mac, were in dire need of regulation. They proposed moving the regulation of these two companies under a new agency within the Department of Treasurey. However, democrats strongly opposed this move and killed the bill in committee.

Democrat Representative Barney Frank said at the time, "These two entities -- Fannie Mae and Freddie Mac -- are not facing any kind of financial crisis, the more people exaggerate these problems, the more pressure there is on these companies, the less we will see in terms of affordable housing."

Democrat Representative Mel Watt also stated at the time, "I don't see much other than a shell game going on here, moving something from one agency to another and in the process weakening the bargaining power of poorer families and their ability to get affordable housing."

The link between illegal immigration and the housing crisis only furthered when congress passed its $800 billion dollar bailout. Representative Michele Bachmann blew the whistle first:

"At the same time that the American taxpayer was being asked to bail these companies out, Barney Frank, the chairman of the Financial Services Committee, instituted a sort of tax on Freddie and Fannie, and that tax goes into what's called an affordable housing trust fund," explains Bachmann. "It's a really a taxpayer-subsidized housing fund, but that money will go to organizations like La Raza and...ACORN."

Both La Raza and ACORN have been strong advocates of illegal immigrant home ownership and have been tied to voter fraud.

If congress fails to recognize the substantial role illegal immigration has played in the current financial crisis they will only continue to make the same disastrous mistakes in the future.

http://thekansascitian.blogspot.com/...-subprime.html

Support our FIGHT AGAINST illegal immigration & Amnesty by joining our E-mail Alerts at https://eepurl.com/cktGTn

-

08-11-2017, 09:10 AM #12Super Moderator

- Join Date

- May 2005

- Location

- Heart of Dixie

- Posts

- 36,012

ILLEGAL ALIENS & THE MORTGAGE MESS

By Michelle Malkin

September 24, 2008 | 7:51am

AS panicked politicians prepare to fork over $1 trillion in taxpayer funding to rescue Wall Street, theyve fingered regulation, deregulation, Fannie Mae and Freddie Mac, the Community Reinvestment Act, Jimmy Carter, Bill Clinton, both Bushes, greedy banks, greedy borrowers, greedy short-sellers and minority-home-ownership promoters for blame.

But theres one villain that has slipped notice: how illegal immigration, crime-enabling banks and open-borders Bush policies fueled the mortgage crisis. Its no coincidence that the areas hardest hit by the foreclosure wave Loudoun County, Va., Californias Inland Empire, Stockton and San Joaquin Valley, and Las Vegas and Phoenix also happen to be some of the nations largest illegal alien sanctuaries. Half of the mortgages to Hispanics are subprime. A quarter of all those subprime loans are in default and foreclosure.

Regional reports across the country have decried the subprime meltdowns impact on illegal-immigrant victims. A July report showed that in seven of the 10 metro areas with the highest foreclosure rates, Hispanics were at least one-third of the population; in two of those areas Merced and Salinas-Monterey, Calif. Hispanics comprised half the population. The National Council of La Raza and its Development Fund have received millions in federal funds to counsel their constituents on obtaining mortgages with little to no money down; the group almost succeeded in attaching a $10 million earmark for itself in one of the housing bills passed this spring.

For the last five years, Ive reported on the rapidly expanding illegal-alien home-loan racket. The top banks clamoring for their handouts as their profits plummet, led by Wachovia and Bank of America, launched aggressive campaigns to woo illegal-alien homebuyers. The quasi-governmental Wisconsin Housing and Economic Development Authority guaranteed home loans to illegal immigrants.

The Washington Post noted in 2005: Hispanics, the nations fastest-growing major ethnic or racial group, have been courted aggressively by real-estate agents, mortgage brokers and programs for first-time buyers that offer help with closing costs. Ads proclaim: Sin verificacion de ingresos! Sin verificacion de documento! which loosely translates as, Income tax forms are not required, nor are immigration papers.

Fraudsters also have engaged in house-flipping rings using illegal aliens as straw buyers. Among many examples the FBI cites: a conspiracy in Las Vegas involving a former Nevada First Residential Mortgage Company branch manager who directed loan officers and processors in the origination of 233 fraudulent Federal Housing Authority loans valued at over $25 million. The defrauders made and submitted false employment and income documentation for borrowers; most were illegal immigrants from Mexico. To date, the FBI reported, Fifty-eight loans with a total value of $6.2 million have gone into default, with a loss to the Housing and Urban Development Department of over $1.9 million.

Its the tip of the iceberg. Thanks to lax Bush administration policies allowing illegal aliens to use matricula consular cards and taxpayer-identification numbers to open bank accounts, mortgage fraud has grown. Money-lenders still have no access to a verification system to check Social Security numbers before approving loans.

In an interview about rampant illegal-alien home-loan fraud, a spokeswoman for the US General Accounting Office told me five years ago: Considering the size of Los Angeles, New York, Chicago, Houston and other large cities throughout the United States known to be inundated with illegal aliens, I dont think the federal government is willing to expose this problem for financial reasons as well as for fear of political repercussions.

The chickens are coming home to roost. Law-abiding taxpayers are going to pay for it.

http://nypost.com/2008/09/24/illegal...mortgage-mess/Support our FIGHT AGAINST illegal immigration & Amnesty by joining our E-mail Alerts at https://eepurl.com/cktGTn

-

08-11-2017, 11:30 AM #13Administrator

- Join Date

- Nov 2004

- Location

- Gheen, Minnesota, United States

- Posts

- 67,790

Final website checks needed at ALIPAC.us Please

https://www.alipac.us/f8/final-websi...please-349572/

Join our efforts to Secure America's Borders and End Illegal Immigration by Joining ALIPAC's E-Mail Alerts network (CLICK HERE)

-

08-11-2017, 05:35 PM #14Moderator

- Join Date

- Apr 2016

- Posts

- 31,077

END DACA NOW!!!

NO PATH TO STAY, NO AMNESTY, DEPORT THEM ALL

STOP THIS FINANCIAL DRAIN ON OUR COUNTRY AND TAXPAYER'SILLEGAL ALIENS HAVE "BROKEN" OUR IMMIGRATION SYSTEM

DO NOT REWARD THEM - DEPORT THEM ALL

-

08-11-2017, 06:48 PM #15Senior Member

- Join Date

- Feb 2017

- Posts

- 1,794

Amen to that! Originally Posted by posylady

Originally Posted by posylady

-

08-11-2017, 07:30 PM #16Super Moderator

- Join Date

- May 2005

- Location

- Heart of Dixie

- Posts

- 36,012

It is worse than you think poseylady and 6 million dollar man. In fact it is, in my opinion, criminal

The original link to this article from Channel 9 is now a 404 error. But, here it is in it's entirety from the ALIPAC archives.(The primary reason that we ask y'all to post the entire article )

)

Time has buried a lot of this, but please do some research on your own. These programs have been funded with Billions of dollars from the bail out and American taxpayers.

The thread is

New plan gives government "grantees" first dibs on

https://www.alipac.us/f19/new-plan-g...t-dibs-202028/

It should be noted that one of the "grantees" is LaRaza. Also, I could not find anything that requires the grantee's clients to be be legal citizens before receiving these 50,000.00 GRANTS to buy the foreclosed homes of people that were forced out of their jobs. Complete redistribution.

eighborhood Stabilization Program GrantsNew plan gives government "grantees" first dibs onIt is one way of very quickly "changing America. Kill the jobs of the middle class, take their home and then give them to the folks that you want to live there. JMO"

New plan gives government first dibs on foreclosures

Kyle Clark

9WANTS TO KNOW

AURORA - A new program allows government agencies and their partners to have exclusive purchase rights on foreclosed homes before families, investors and the rest of the private market is allowed to bid.

9Wants to Know has learned the initiative, called First Look, is touted as a tool to maximize an effort funded with federal taxpayer dollars to fix-and-flip homes in distressed neighborhoods.

Critics argue First Look is government intrusion into the real estate marketplace that will impact families looking to purchase and live in a foreclosed house.

Charles Roberts, a Realtor with Your Castle Real Estate in Denver, called the recently-announced government initiative "appalling."

"They're changing the rules. They're tilting it in their favor," Roberts said. "They actually get an opportunity to buy a house before a homeowner, which doesn't make any sense to me at all."

First Look will be utilized by grantees in the Department of Housing and Urban Development's Neighborhood Stabilization Program (NSP).

Since 2008, the NSP has used billions in federal tax money with the aim of shoring up troubled neighborhoods plagued by foreclosures and abandoned homes. The homes are resold to low-income and moderate-income families at or below the cost to the government or participating non-profit.

First Look offers NSP grantees including state and local governments and non-profit organizations an exclusive one to two day window to express interest in a property. Those governments and nonprofits will have five to 12 days to close the deal before the property is opened to the private market.

The initiative is a partnership between HUD, the Stabilization Trust and financial institutions holding an estimated 75 percent of the bank-owned properties in the U.S.

An additional $1 billion in taxpayer money was recently infused into the NSP by a financial reform bill passed by Congress. At a Sept. 8 news conference in Aurora, HUD officials announced $17.3 million of that funding is designated for use in Colorado.

"This first look is really a game changing approach, market-oriented and cost-effective," Regional HUD Director Rick Garcia said.

Realtor Jude Sandvall laughed at that description.

"I don't understand how the government having the ability to purchase properties before individuals and families is a market-oriented approach," Sandvall said. "They're taking those families' taxpayer dollars and purchasing properties before those families even have an opportunity to look at those properties and purchase them."

At the HUD news conference, Garcia defended giving governments and their partner organizations exclusive first access as an issue of "who knows best."

"Who knows best but the local people running these programs, and particularly those in the City of Aurora, about how to get these properties back on the market?" Garcia said.

"I would ask the same question: 'Who do you think knows best?'" Roberts said. "I think the answer is exactly the opposite of what he would like you to think."

The latest $1 billion in NSP funding is expected to impact 14,000 foreclosed homes nationwide. Colorado alone had 20,437 foreclosures in 2009. HUD officials say sheer numbers mean the impact of First Look will be limited.

"There are still a tremendous number of foreclosed properties that are available on the market to the private sector," Garcia told 9Wants to Know investigator Kyle Clark.

HUD spokesman Brian Sullivan says the foreclosures purchased through First Look will only be in troubled neighborhoods, but acknowledged that local governments and nonprofits will determine which neighborhoods qualify.

"It's a preference that serves a larger public purpose," Sullivan said of First Look, calling it a "minor and highly temporary inconvenience" to those in the open market.

Critics say they're not concerned about local governments and their partners taking a large quantity of the foreclosed properties. Their concern is rooted in issued of principle and priority.

"The government has mandated they get the best properties," Roberts said. "It seems incredibly unfair."

(KUSA-TV © 2010 Multimedia Holdings Corporation)

http://www.9news.com/news/article.aspx? ... &catid=339

HUD Announces Allocation of $1 billion in NSP3 Funding

Introduction

The Neighborhood Stabilization Program (NSP) was established for the purpose of stabilizing communities that have suffered from foreclosures and abandonment. Through the purchase and redevelopment of foreclosed and abandoned homes and residential properties, the goal of the program is being realized. NSP1, a term that references the NSP funds authorized under Division B, Title III of the Housing and Economic Recovery Act (HERA) of 2008, provides grants to all states and selected local governments on a formula basis. NSP2, a term that references the NSP funds authorized under the American Recovery and Reinvestment Act (the Recovery Act) of 2009, provides grants to states, local governments, nonprofits and a consortium of nonprofit entities on a competitive basis. The Recovery Act also authorized HUD to establish NSP-TA, a $50 million allocation made available to national and local technical assistance providers to support NSP grantees.

NSP Resource Exchange

NSP Resource Exchange is a one-stop shop for the information and resources needed by NSP grantees, subrecipients and developers to purchase, rehabilitate, and resell foreclosed properties. There are three primary components to the Resource Exchange site including:

Find a Resource - a database of policy guidance, practitioner support tools and training materials developed by HUD and technical assistance providers who specialize in NSP-related activities. It can be browsed by topic, audience, or type of information.

Ask a Question a feature that can be used to direct users to previously asked questions based on the userâs questions. It also provides users with a question form that can be submitted electronically for those questions and answers that are not listed on the website.

Request TA a mechanism by which users can communicate with technical assistance providers and request support in implementing NSP activities

The NSP Resource Exchange can also be used to learn about upcoming events related to NSP and coming soon the site will feature tool kits for designing programs and implementing activities.

Nature of Program

NSP is a component of the Community Development Block Grant (CDBG). The CDBG regulatory structure is the platform used to implement NSP and the HOME program provides a safe harbor for NSP affordability requirements.

NSP grantees develop their own programs and funding priorities. However, NSP grantees must use at least 25 percent of the funds appropriated for the purchase and redevelopment of abandoned or foreclosed homes or residential properties that will be used to house individuals or families whose incomes do not exceed 50 percent of the area median income. In addition, all activities funded by NSP must benefit low- and moderate-income persons whose income does not exceed 120 percent of area median income. Activities may not qualify under NSP using the "prevent or eliminate slums and blight" or "address urgent community development needs" objectives.

Eligible Uses

NSP funds may be used for activities which include, but are not limited to:

Establish financing mechanisms for purchase and redevelopment of foreclosed homes and residential properties;

Purchase and rehabilitate homes and residential properties abandoned or foreclosed;

Establish land banks for foreclosed homes;

Demolish blighted structures;

Redevelop demolished or vacant properties

Homebuyer Assistance

Homebuyers cannot receive assistance directly from HUD. NSP funds can be used to help homebuyers purchase homes, but they must contact an NSP grantee for application details. NSP operates on a national scale, but participation requirements may differ from one state or city to another. For information on how you may purchase a home with NSP assistance please contact an NSP grantee in your area. See NSP Grantee Contacts page for details.

Contact Us

If you would like additional information on the program please use this form to contact a HUD NSP Representative.

http://www.hud.gov/offices/cpd/communit ... orhoodspg/

NSP grantees get first chance to buy HUD Homes at 10 percent discountPosted by Laura Williams on July 14, 2010 at 9:35am in Neighborhood Stabilization

Back to Neighborhood Stabilization Discussions

In case you haven't seen the release:

FHA ANNOUNCES FIRST LOOK INITIATIVE TO HELP COMMUNITIES STABILIZE NEIGHBORHOODS HARD-HIT BY FORECLOSURE

NSP grantees get first chance to buy HUD Homes at 10 percent discount

WASHINGTON - The U.S. Department of Housing and Urban Development (HUD) today announced a new initiative that gives state and local governments, and

nonprofit organizations participating in HUD's Neighborhood Stabilization

Program (NSP) preference to acquire homes from the Department's inventory

of foreclosed properties, commonly known as "HUD homes." The

initiative was announced by HUD Secretary Shaun Donovan at the National Council

of La Raza annual conference in San Antonio, Texas.

http://forum.housingpolicy.org/group/ne ... e=activity

Additionally, the government gave them a discount and addition Grants to

"fix them up" that didn't have to be repaid if they lived there 7 years.

The Trump Administration had better fix this NOW, but it doesn't help those people that lost their homes and wound up in tent cities all over the country while the "more deserving" moved into their homes, IMO.Support our FIGHT AGAINST illegal immigration & Amnesty by joining our E-mail Alerts at https://eepurl.com/cktGTn

-

08-11-2017, 08:23 PM #17Senior Member

- Join Date

- Aug 2008

- Location

- PARADISE (San Diego)

- Posts

- 99,040

NO AMNESTY

Don't reward the criminal actions of millions of illegal aliens by giving them citizenship.

Sign in and post comments here.

Please support our fight against illegal immigration by joining ALIPAC's email alerts here https://eepurl.com/cktGTn

-

08-11-2017, 08:36 PM #18Senior Member

- Join Date

- Aug 2008

- Location

- PARADISE (San Diego)

- Posts

- 99,040

I just found this in ALIPAC archive.

@ https://www.alipac.us/f9/can-illegal...operty-230158/

-----------------------------

Banks are Quietly Wooing Undocumented Immigrants

Many illegal aliens are hard-working, tax-paying U.S. citizen wannabes-and banks are banking on their desire to be homeowners, too. And why not? There's no law against it.

US Banker | June 2005

By Steve Bergsman

As Washington signals a more lenient immigration policy toward the nation's eight million to 11 million undocumented aliens, U.S. banks like Fifth Third, North Shore Bank and Second Federal Savings & Loan, are quietly courting this group for home mortgages.

"Banks are not an arm of the immigration department," says Kevin Mukri, a spokesperson for the Office of the Comptroller of the Currency, the primary bank regulator. "As long as those getting mortgages meet the requirements of being authorized bank customers, including proper ID, it would be discriminatory not to service them." There is no law against banks issuing mortgages to illegal immigrants, nor against their owning property in the U.S.

An estimated six million to eight million of those undocumented are Latinos, who alone represent a potential $44 billion market in homes, according to the National Association of Hispanic Real Estate Professionals.

The Federal Deposit Insurance Corp. and the Mortgage Guaranty Insurance Corp., a Milwaukee-based mortgage insurer, recently gave their blessing to a product aimed at this group, the ITIN mortgage. An acronym for the Income Tax Identification Number, the ITIN mortgage is marketed to those with the nine-digit Internal Revenue Service number. Working illegal immigrants seek an ITIN number for tax-paying purposes because they aren't eligible for a Social Security number. Both resident and nonresident aliens may have ITIN numbers. Michael Frias, an FDIC spokesman, confirms that banks aren't legally required to verify legal status. "There is no federal banking law that requires banks to verify the immigration status of foreign account holders," he says.

Don Cohen, vp of community lending for North Shore Bank of Brookfield, WI, has been offering ITIN mortgages since September. "This is a whole new market," he says. "Immigrants are hard working, earn income, have down-payment money and want to own a home." If an illegal alien is deported and defaults on his mortgage, the bank would own the home.

Last autumn, the MGIC began working with 35 lenders to offer mortgage insurance for ITIN mortgages, an endorsement that cuts the loans' interest rates, and to date it has insured 196 loans worth more than $25 million. "We recognize the reality of a standing immigrant population," says Ryan Daniels, a spokesman for MGIC. He acknowledges that many in this target audience may be undocumented, but underwriting standards only require that applicants have an ITIN number and have paid taxes for at least two years. Not one of its 196 loans has been delinquent, he says.

The growth of ITIN mortgage programs shows how banks have adapted to the economic reality of illegal immigrants, many of whom aren't deported by the Immigration and Naturalization Service unless they commit violent crimes. Although it's illegal to hire them, few employers are prosecuted, and the IRS accepts their tax payments. Moreover, many households with an undocumented immigrant also may include a legal permanent resident or U.S. citizen, frequently a child born here. "Anything that accommodates their illegal presence encourages them to stay and others to come," warns Jack Martin, special projects director for the Federation for American Immigration Reform in Washington, D.C.

For the most part, however, banks are staying out of the political fray, and concentrating on business strategy. Second Federal Savings & Loan, based in the Chicago area, has offered ITIN mortgages for several years, but has renewed its focus in the last 18 months. "With margins narrowing, we got squeezed," says president and CEO Mark Doyle. "We looked at our alternatives. One glaring opportunity was in the ITIN market." It proved to be a solid bet: Today, the bank's $70 million ITIN portfolio is "performing well" with no foreclosures, he says, though he declined to provide profit figures.

Doyle says illegal immigrants have proven to be no bigger risk than legal immigrants or U.S. citizens. North Shore Bank's Cohen concurs, saying, "The risk has been minimal to non-existent."

In November, Cincinnati-based Fifth Third Bancorp introduced an ITIN mortgage in seven markets, drawing twice the number of expected candidates. Says Bill Schumer, vp of product development, "This is a great outlet to help Hispanics establish roots here."

Other financial institutions offering the mortgages include Banco Popular in Houston; Self-Help Credit Union in Durham, NC; First Bank of the Americas in Chicago; Texas Bank in Fort Worth, TX; and Mitchell Bank of Milwaukee.

http://www.us-banker.com http://www.sourcemedia.com

http://www.americanbanker.com/usb_issue ... 351-1.htmlLast edited by JohnDoe2; 08-11-2017 at 08:40 PM.

NO AMNESTY

Don't reward the criminal actions of millions of illegal aliens by giving them citizenship.

Sign in and post comments here.

Please support our fight against illegal immigration by joining ALIPAC's email alerts here https://eepurl.com/cktGTn

-

08-11-2017, 10:04 PM #19Super Moderator

- Join Date

- May 2005

- Location

- Heart of Dixie

- Posts

- 36,012

Good find JD2. When I checked the link it is now a 404 (scrubbed) Good thing we have the archives...

Support our FIGHT AGAINST illegal immigration & Amnesty by joining our E-mail Alerts at https://eepurl.com/cktGTn

-

08-11-2017, 11:42 PM #20Senior Member

- Join Date

- Mar 2006

- Posts

- 7,377

Some years ago, maybe 15, I read two different article, some weeks apart, in the Dallas paper,concerning illegals and mortgages.

It was interviews with 2 different HUD officials, and they both essentially said so many illegals have mortages through HUD, if they defaulted, HUD would go under.

Also, maybe 25 years ago, in a small town with poultry industry and a lot of illegals, I talked with a real estate agent. She said she had been so busy because the government had made it OK for illegals to buy houses, and she was closing an average of 18 sales a day for the last month!!!

This is a town of approx 9/10K people.

Reply With Quote

Reply With QuoteSimilar Threads

-

We have a disease. Its infecting every aspect of our society and its time we did so

By AirborneSapper7 in forum General DiscussionReplies: 17Last Post: 11-21-2014, 11:17 PM -

Here Come the Taxes: In Every Aspect of our Lives

By kathyet in forum Other Topics News and IssuesReplies: 0Last Post: 11-07-2012, 01:21 PM -

Illegal Alien FirefightersâThe Financial Aspect

By zeezil in forum illegal immigration News Stories & ReportsReplies: 7Last Post: 08-13-2008, 10:11 PM -

Elections in Italy (immigration aspect)

By Lugundum in forum Other Topics News and IssuesReplies: 0Last Post: 04-13-2008, 08:53 AM -

Voting: the most precious, revered aspect of citizenship

By Feck in forum General DiscussionReplies: 2Last Post: 01-20-2008, 03:27 AM

We must push through early Thurs at this critical moment

04-24-2024, 10:44 PM in illegal immigration Announcements