Results 1 to 1 of 1

Thread Information

Users Browsing this Thread

There are currently 1 users browsing this thread. (0 members and 1 guests)

LinkBack URL

LinkBack URL About LinkBacks

About LinkBacksHybrid View

-

09-21-2009, 08:57 AM #1Senior Member

- Join Date

- May 2007

- Location

- South West Florida (Behind friendly lines but still in Occupied Territory)

- Posts

- 117,696

Is Pent-Up Inflation From Fed Printing Waiting On Deck?

Is Pent-Up Inflation From Fed Printing Waiting On Deck?

Inquiring minds are wondering about the possibility of "pent-up" inflation from the massive expansion money supply by the Fed. Our search for the truth starts with the question "Which Comes First: The Printing or The Lending?"

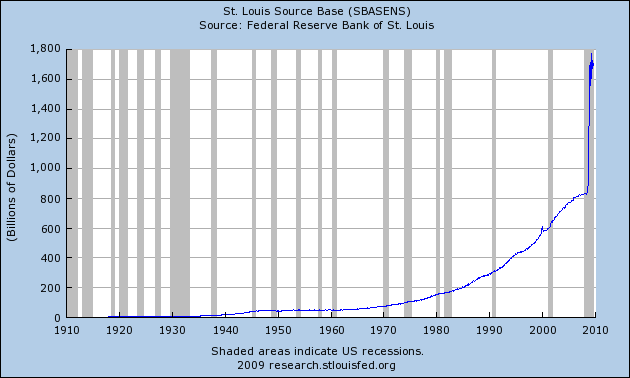

This is a critical question given the massive expansion of base money by the Fed as shown in the following chart.

Base Money Supply

Since the beginning of the recession, the Fed has expanded base money supply from $800 billion to $1.7 trillion. Conventional wisdom suggests this money is going to come soaring into the economy at any second causing hyperinflation on the notion banks will lend out 10 times the amount of reserves.

So is this pent-up inflation just waiting to break out?

Hardly.

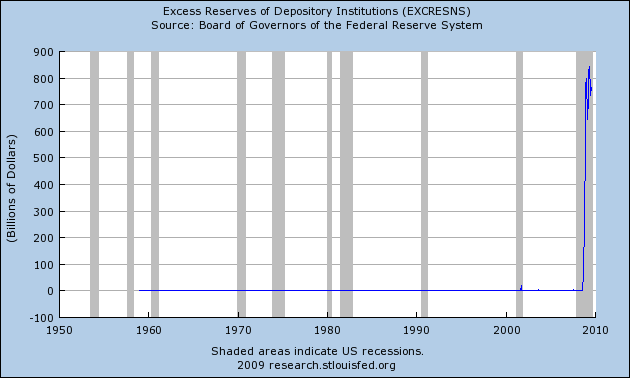

A funny thing happened to the inflation theory: Banks aren't lending and proof can be found in excess reserves at member banks.

Excess Reserves

Banks are Insolvent, Consumers Tapped Out

Because of rising credit card defaults, commercial real estate defaults, foreclosures, walk-aways, and other bad debts, banks need those reserves to cover future losses.

In practice, banks are insolvent, unable or unwilling to lend. Moreover, tapped out consumers are unable or unwilling to borrow. As a result, Spending Collapses In All Generation Groups. http://globaleconomicanalysis.blogspot. ... ation.html

Bernanke can flood the world with "reserves" and indeed he has. However, he cannot force banks to lend or consumers to borrow.

Yet every day someone comes up with another convoluted theory about how inflationary this all is. It is certainly "distortionary" in that it creates problems down the road and prolongs a real recovery by keeping zombie banks alive (as happened in Japan). However, it is not (in aggregate) going to cause massive inflation because it is not spurring the creation of new debt.

Consumers and banks both are suffering from a massive hangover. Their willingness and ability to drink is gone. No matter how many pints of whiskey Bernanke sets in front of someone passed out on the floor, liquor sales will not rise.

In a debt-based economy, it is extremely difficult to produce inflation if consumers will not participate. And as noted above, demographics and attitudes strongly suggest consumers have had enough of debt and spending sprees.

Those pointing to flawed measures of money supply as proof of inflation just don't get it, and likely never will.

Banks Lend, Reserves Come Later

In practice, banks lend money and reserves come later. When defaults pile up, the Fed prints reserves to cover bank losses. Thus, those "excess reserves" aren't going anywhere. They are needed to cover losses. It's best to think of those reserves as a mirage. They don't really exist.

In the meantime, the Fed is pretending banks are solvent and banks are pretending they are well capitalized. Furthermore, in a world of falling asset prices and rampant overcapacity, banks have little reason to lend even if they were solvent.

These are simple concepts, yet few understand them. Australian economist Steve Keen is one of few who do. Some don't want to understand because it shatters their hyperinflation dreams.

Steve Keen On the Edge

On Friday, Steve Keen was On the Edge with Max Keiser discussing these issues.

http://www.youtube.com/watch?v=VoqaMzBK ... r_embedded

Did The Government Rescue The System?

Steve Keen has a "debtwatch" blog that's well worth following. Please consider Itâs Hard Being a Bear (Part Five): Rescued? http://www.debtdeflation.com/blogs/2009 ... e-rescued/

In explaining his recovery program http://www.nytimes.com/2009/04/14/us/po ... .html?_r=1 in April, President Obama noted that:

âthere are a lot of Americans who understandably think that government money would be better spent going directly to families and businesses instead of banks â âwhereâs our bailout?,â they askâJoin our efforts to Secure America's Borders and End Illegal Immigration by Joining ALIPAC's E-Mail Alerts network (CLICK HERE)

Reply With Quote

Reply With Quote

Migrants Breach Fortified Border Barrier, March Through Texas...

05-16-2024, 08:20 PM in illegal immigration News Stories & Reports